ETF Fees vs Mutual Fund Fees in Canada: A $179,307 Difference on the Same $100K Portfolio

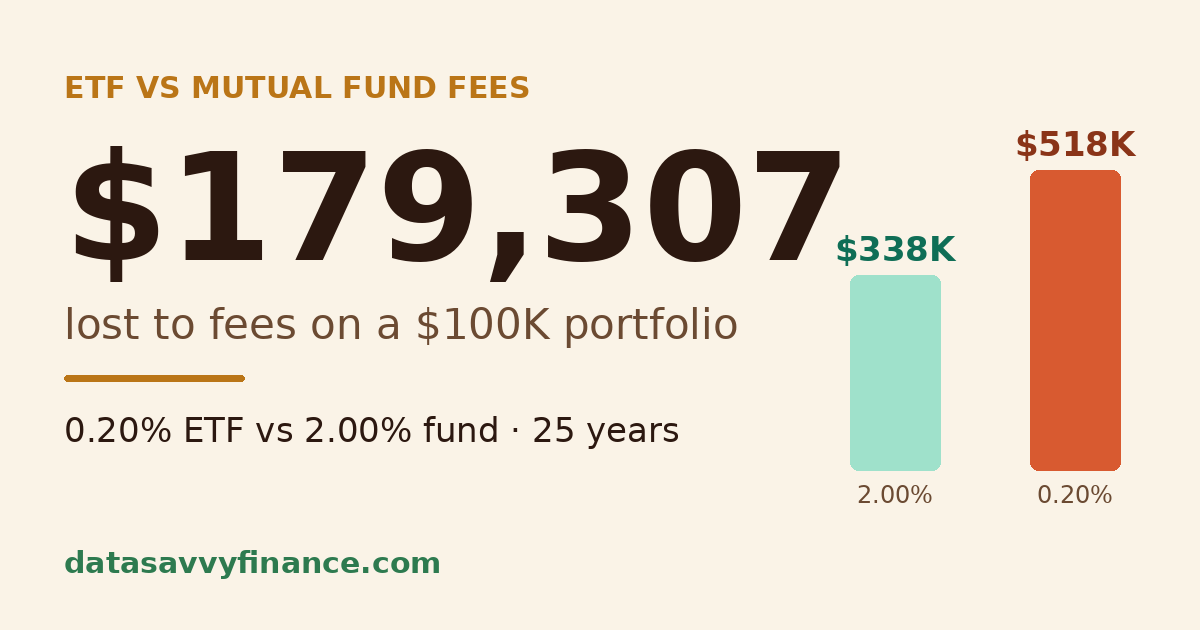

Here is the number most Canadian investors have never actually seen written out. A $100,000 portfolio held for 25 years in a low-cost ETF at 0.20% MER grows to $517,942. The same portfolio in an average bank mutual fund at 2.00% grows to $338,635. The gap is $179,307, not fees paid, but portfolio value that never existed because it was quietly consumed by fees.

Educational Disclaimer: The ETFs, funds, and financial products discussed on this website are provided as real-world educational examples to illustrate investing concepts and portfolio fee structures. They are not individualized investment recommendations or endorsements. Comparable products from other providers may exist.

The Weekend Fee Audit

On a $100,000 portfolio over 25 years, the gap between a 0.20% ETF and a 2.00% fund is $179,307. Four steps, about 20 minutes, and you’ll know where your own number lands.

You don’t need an advisor, a spreadsheet, or any math to run this. You need your last statement and a browser tab. (Figures: $100K, 7% gross return, 25 years, lump sum. Add your monthly contributions in the calculator.)

-

☐ Step 1. Find your MER. (5 min)

Open the Fund Facts document for every fund you hold. The MER is on page 1, as a percentage. Your provider’s site and Morningstar Canada both list it. Write it down. Three funds, three numbers. -

☐ Step 2. Find your balance. (2 min)

Your last statement. One number per account. -

☐ Step 3. Run the gap. (10 min)

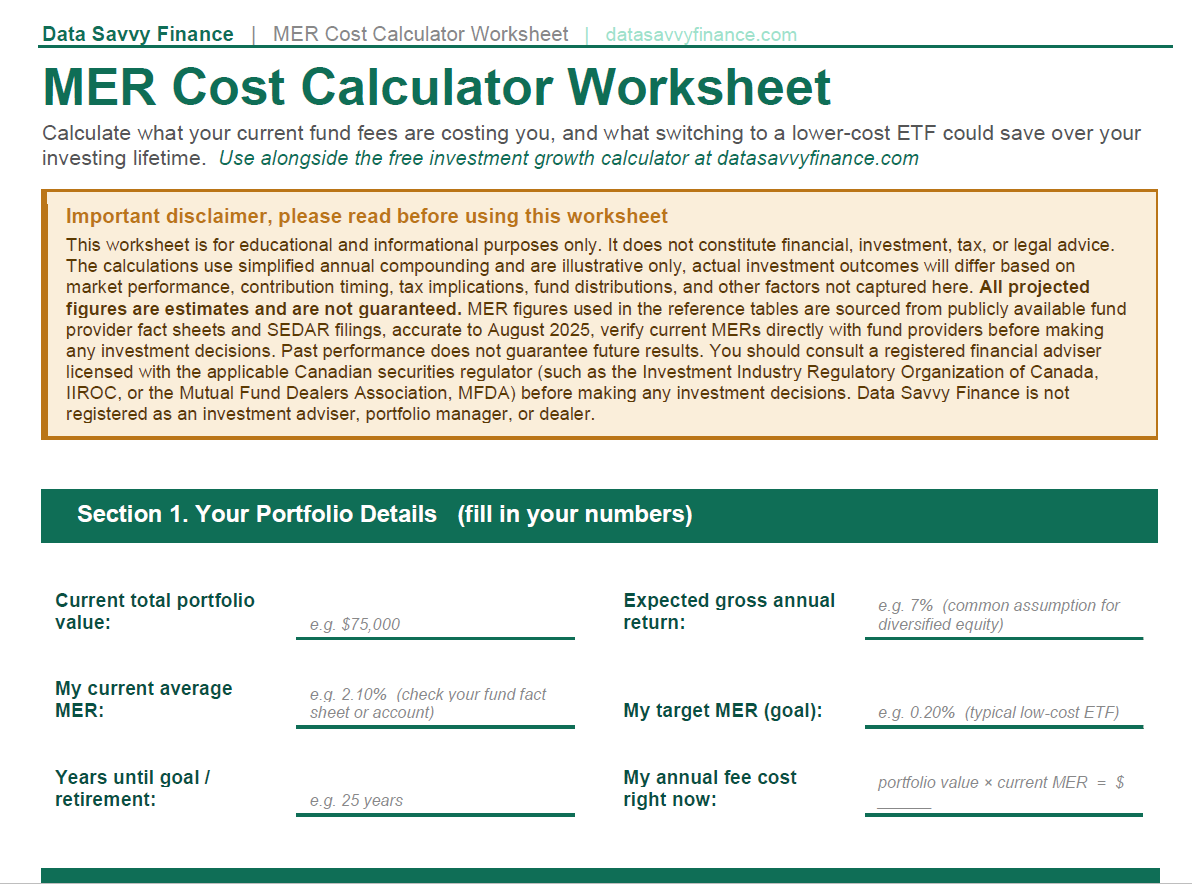

Enter your balance and MER in the worksheet below. It shows the dollar gap between your fee and a 0.20% ETF over 25 years — $179,307 on a $100K portfolio. Investing monthly too? The investment growth calculator adds your contributions. -

☐ Step 4. Check your account type. (3 min)

RRSP vs TFSA vs non-registered changes the fee drag. The worksheet flags it.

Get your number in 4 boxes

Enter your balances and current MER. Get your real all-in cost and your 25-year fee drag. About 10 minutes, no signup for the checklist.

ETF Fees vs Mutual Fund Fees in Canada: The Real Cost Difference (2026)

I remember the first time I actually ran the numbers. Not the percentage, the dollar figure. I had known for years that ETFs were cheaper than mutual funds. I did not know by how much until I sat down with a calculator and modelled it out over 25 years. The result was more concrete than anything I had read about fees before.

The average Canadian equity mutual fund charges a management expense ratio of 2.0 to 2.5%. The average Canadian ETF charges 0.20 to 0.35%. On a $100,000 portfolio over 25 years, assuming identical 7% gross annual returns, that fee difference reduces your ending portfolio value by approximately $150,000 to $200,000.

That is not the total amount paid in fees. That is the compounded portfolio value that never existed because it was quietly consumed by fees, year after year, before you ever saw it.

Most Canadian investors know their mutual fund has fees. Very few have seen what those fees actually cost in dollar terms over a lifetime of investing. The financial industry has a structural incentive to keep that calculation abstract, expressed as a small percentage rather than a large number. This article does the calculation clearly and applies it to realistic Canadian scenarios.

What Are Investment Fees and Why Do They Matter?

Every investment fund, whether a mutual fund or an ETF, charges an annual fee to cover the cost of running it. That fee is expressed as a percentage of your total investment and is called the management expense ratio, or MER.

The mechanics matter. The fee is not billed to you separately. It is deducted from the fund’s assets before performance is reported, which means you never see it leave your account. If a fund earns 7% before fees and charges a 2% MER, you see 5%. The 2% is simply gone, silently, every year.

That invisibility is part of why the fee problem persists. Most Canadian investors holding bank mutual funds have never calculated what their MER costs them in dollar terms over 20 or 30 years. They see a percentage. They don’t see the compounding effect of that percentage applied to a growing balance year after year, over decades.

Here is the key insight that makes fees so damaging at scale. A fee taken out in year one doesn’t just cost you that dollar. It costs you every dollar that dollar would have compounded into over the remaining years of your investment horizon. A 2% fee on a $100,000 portfolio costs $2,000 in year one. But that $2,000 your portfolio has lost in year 1, could have compounded to $10,800 over 25 years, assuming 7% overall investment horizon average return. The fee doesn’t just reduce your balance today. It reduces every future return that balance would have generated.

For a detailed explanation of how MER is calculated and what it actually includes, see how the management expense ratio impacts your investment returns.

For a clear benchmark of what a reasonable fee looks like, see what is a good MER for ETFs in Canada.

Canadian Mutual Fund Fees, What You’re Actually Paying

Canada has some of the highest mutual fund fees in the developed world. That is not an opinion, it is a data point that has been documented consistently for over a decade.

According to data from the Investment Funds Institute of Canada cited in a Conference Board of Canada report via Investment Executive, the average asset-weighted MER for Canadian mutual funds was 1.47% as of 2023. That figure includes lower-cost fee-based series funds that bring the average down. The mutual funds most Canadians actually hold through their banks, the Series A funds sold through branch advisors, routinely carry MERs of 2.0 to 2.5%.

What does the MER actually pay for?

A typical 2% mutual fund MER breaks down roughly as follows:

- Portfolio management: approximately 0.50 to 0.75%

- Trailing commission to the advisor who sold and services the fund: approximately 0.75 to 1.00%

- Administration, legal, regulatory, and marketing costs: approximately 0.25 to 0.50%

The trailing commission is the part most Canadian investors don’t know about. Roughly half of the MER on a typical bank mutual fund flows directly to the financial advisor or branch representative who recommended it, paid as an ongoing annual commission for as long as you hold the fund. This creates a structural conflict of interest, where advisors have a financial incentive to keep clients in higher-fee products regardless of whether those products are in the client’s best interest.

Here are some real MERs from commonly held Canadian bank funds, for illustrative context. Always verify current figures on the fund provider’s website before making any decisions:

- RBC Select Balanced Portfolio Series A: approximately 1.94%

- TD Balanced Growth Fund Series A: approximately 2.23%

- Scotiabank DynamicEdge Balanced Portfolio: approximately 2.21%

These are not outliers. They are representative of what millions of Canadians are currently paying to hold funds they bought at a bank branch, often without fully understanding what the fee structure involves.

For investors who are actively using their advisor for financial planning, tax guidance, and behavioural coaching during market volatility, a portion of that fee has real value. For investors who bought a balanced fund at a bank branch years ago and have had no meaningful advisor contact since, the trailing commission is paying for a service that is not being delivered.

See what is a good MER for ETFs in Canada for context on what a competitive fee looks like.

Canadian ETF Fees, What You Pay Instead

The fee structure for ETFs is fundamentally different from mutual funds, and the difference is not subtle.

A Canadian ETF tracking a broad market index has no portfolio manager making active decisions, no research team generating buy and sell recommendations, and no trailing commission flowing to an advisor. The fund simply holds the securities in its index, rebalances mechanically when the index changes, and passes the cost savings directly to investors. That stripped-back structure is why the fees are so much lower.

The all-in-one ETFs are worth noting specifically. A single fund at 0.20% gives a Canadian investor exposure to thousands of companies across global equity markets, automatic rebalancing, and a diversified portfolio that would have cost 10 times more inside a typical Canadian bank balanced fund.

One cost worth flagging for transparency. Self-directed ETF investing through a brokerage means placing your own trades. Some platforms charge commissions per trade, which matters for investors making small, frequent purchases. Some Canadian discount brokerages offer commission-free ETF purchases or zero-commission trading on all securities, verify current trading terms on each platform’s website before selecting one.

For a full breakdown and an illustration of how to structure low-cost ETF portfolio using funds like these, see the 3-ETF portfolio guide for Canadian investors.

The Real Cost Difference, 25-Year Comparison

Percentages are abstract. Dollar figures are not. Here is what the fee difference actually looks like over a realistic investing horizon.

The three scenarios below use a $100,000 starting balance, $500 monthly contributions, and a 7% gross annual return over 25 years. The only variable is the MER.

The three scenarios below in Figure 1 and Table 1 use a $100,000 starting balance, $500 monthly contributions, and a 7% gross annual return over 25 years. The only variable is the MER.

| Scenario | MER | Net return | Ending value |

| Low-cost ETF portfolio | 0.20% | 6.80% | $548,673 |

| Average Canadian mutual fund | 2.00% | 5.00% | $362,499 |

| High-cost bank equity fund | 2.50% | 4.50% | $322,826 |

Table 1. Illustration of how investment costs affect investment growth over a 25 year investment horizon.

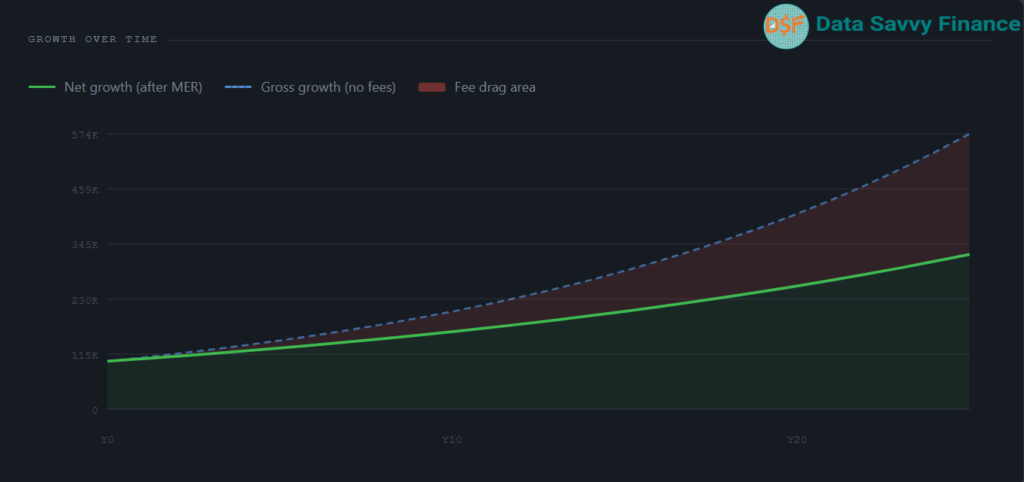

The gap between the ETF scenario and the average mutual fund scenario is the number worth focusing on. That difference is not the total fees paid over 25 years. It is the ending portfolio value that never existed because the compounding engine was running on a smaller balance every single year.

What if you started with less?

The percentage gap is identical regardless of starting balance, but the dollar figures become more accessible for investors earlier in their journey. Running the same comparison with a $10,000 starting balance and $200 monthly contributions produces a smaller absolute gap but the same structural conclusion: the fee difference compounds into a significant sum over any 25-year period.

The honest framing is this. You cannot control what markets return. You cannot predict which sectors will outperform. But the fee you pay is a number you can see, compare, and choose before you invest a single dollar. It is one of the few genuine edges available to any investor regardless of experience or knowledge.

Run your own comparison using the investment growth calculator with your actual starting balance, monthly contribution, and time horizon.

What Are You Getting for the Higher Fee?

This is the question worth asking honestly before drawing conclusions. A 2% MER is not inherently unjustifiable. It depends entirely on what you are receiving in exchange for it.

If you have an active advisory relationship

Some Canadian investors have genuine, ongoing relationships with financial advisors who provide tax planning, estate planning, insurance guidance, and behavioural coaching through market volatility. For those investors, the embedded advisor commission within the mutual fund MER has real value. The question is not whether the fee structure is fair in principle, but whether you are actually receiving the service it is meant to fund.

When the advisory relationship is limited or inactive

For investors with limited or no ongoing advisor contact, the trailing commission built into the Series A MER continues to be deducted regardless of the level of service received. This is a structural feature of how embedded-commission mutual funds work, not a judgment about any individual advisor relationship. Whether that structure represents fair value in a given situation is a question each investor needs to assess for themselves.

The fee-based advisor alternative

Some advisors operate on a transparent fee-for-service model and use F-series mutual funds, which strip out the embedded commission. F-series MERs typically run 0.80 to 1.10%, meaningfully lower than Series A but still higher than a self-directed ETF portfolio. The advantage is transparency, the fee is visible and tied directly to services received rather than embedded invisibly in the product.

The honest conclusion is straightforward. For a self-directed investor who manages their own portfolio and does not use an advisor, paying 2% annually means paying for a service that is not being delivered. For an investor with an active, valuable advisory relationship, the calculus is more nuanced.

The Switching Cost, What Happens When You Move

The most common reason investors stay in high-fee mutual funds longer than they should is not conviction. It’s inertia, and the sense that the switching process is complicated. Here is what it actually involves.

Does transferring trigger capital gains?

Inside a TFSA or RRSP, transferring from mutual funds to ETFs has zero tax consequences. The transfer happens within a registered account and no taxable event is triggered regardless of how much the fund has appreciated. This is the most important point for most Canadian investors, because the majority of long-term savings sit in registered accounts.

One important caution here: do not withdraw the funds yourself and then re-deposit them at the new brokerage. Doing that counts as a withdrawal from your registered account, which can trigger taxes and permanently reduce your contribution room. Instead, initiate the transfer directly through your chosen brokerage and let them request the account from your bank on your behalf. The receiving institution handles the logistics, you do not need to contact your bank directly.

Inside a non-registered account the situation is different. Selling a mutual fund that has appreciated triggers a capital gains event on the gain. The practical strategy is to prioritise switching registered accounts first, where the fee reduction is immediate, permanent, and completely tax-free.

How does the transfer actually work?

You fill out a transfer form at your new brokerage. They contact your bank directly and handle the logistics. You do not need to call your bank, sell anything yourself, or manage the process. The typical timeline is 5 to 10 business days. Your bank will likely charge a transfer-out fee of $100 to $150 per account. Questrade covers transfer-in fees up to $150 per account, which in most cases makes the switch effectively free.

What about deferred sales charges?

The Canadian Securities Administrators banned the sale of new deferred sales charge mutual funds in June 2022. Investors who purchased DSC funds before the ban may still have active redemption schedules with early withdrawal penalties. Check your fund facts document or contact your advisor before switching any existing DSC fund holdings.

For a full comparison of platforms that support transfers from bank mutual funds, see how Questrade and Wealthsimple handle transfers.

After the Audit: How the Switch Actually Works

This section describes a general process for educational purposes only. It does not constitute financial advice. Your specific tax situation, existing advisor relationship, and account types should inform any decision you make.

- Find your current MER. Check the fund facts document for each fund you hold. It is a standardized disclosure required by Canadian securities regulators and lists the MER clearly on the first page. Your fund provider’s website and Morningstar Canada are also reliable sources.

- Model the long-term cost difference. Use the investment growth calculator with your actual starting balance, monthly contribution, and time horizon. See the dollar gap, not just the percentage gap, before making any decision.

- Prioritise registered accounts. If switching makes sense for your situation, TFSA and RRSP transfers carry no tax consequences. Start there, and remember to not do the withdrawals yourself, this should be handled by your new chosen brokerage.

- Choose a platform and complete a transfer form. Your chosen brokerage handles the transfer of accounts from your bank. Some Canadian brokerages cover transfer-in fees up to a set amount, check current terms on the platform’s website before initiating. For a examples of how major Canadian platforms handle transfers, see the Questrade vs Wealthsimple guide on DatasavvyFinance.com.

For investors who want lower fees than traditional mutual funds but prefer not to self-direct, a robo-advisor like Wealthsimple Invest charges approximately 0.40 to 0.50% annually, still significantly lower than 2%.

For investors who want lower fees than traditional mutual funds but prefer not to self-direct, managed ETF portfolio services at several Canadian brokerages charge approximately 0.40 to 0.70% annually, still significantly lower than 2% Series A mutual funds, though higher than a self-directed ETF approach.

Conclusion

The fee gap between Canadian mutual funds and ETFs is not a minor consideration. It is one of the most significant financial decisions most Canadian investors will ever make, and for most people it is a decision they are making by default rather than by choice.

The numbers are clear. A 2% MER on a Canadian equity fund versus a 0.20% ETF portfolio is not a small difference compounded over 25 years. It is a very large dollar amount that either stays in your portfolio or flows to a fund company and an advisor you may never speak to.

For investors with active advisory relationships, the fee structure has nuance. For self-directed investors holding bank funds out of inertia, the calculation is straightforward.

Model your own numbers using the investment growth calculator. See the dollar figure, not the percentage. Then decide.

This article is for educational and informational purposes only and does not constitute financial, investment, or tax advice. Consult a registered financial advisor before making any investment decisions.

The average asset-weighted MER for Canadian mutual funds was approximately 1.47% as of 2023, according to IFIC data. However, the most commonly held bank equity and balanced funds carry MERs of 2.0 to 2.5%. This is among the highest in the developed world.

The average asset-weighted MER for Canada-listed ETFs was 0.32% as of 2023, according to IFIC data. The most popular Canadian all-in-one ETFs including XEQT and VEQT carry MERs of approximately 0.20%. Single-asset ETFs like ZCN and VFV are even lower at 0.06% to 0.09%.

On a $100,000 portfolio over 25 years at 7% gross annual returns, the difference between a 0.20% ETF portfolio and a 2.00% mutual fund portfolio results in roughly $150,000 to $200,000 less in ending portfolio value. The fee difference is not a minor consideration, it is one of the largest financial decisions most Canadian investors will make.

The data in this article consistently shows that the fee difference between a low-cost ETF portfolio and a high-MER mutual fund compounds into a significant gap in ending portfolio value over long time horizons, $186,174 on the specific scenario modelled here. For self-directed investors, that fee difference is a structural advantage that does not require market timing or stock selection. For investors with active advisory relationships who receive financial planning and tax guidance, the fee structure has more nuance. This article is educational, consult a registered financial advisor for advice specific to your situation.

Yes. MER is charged annually regardless of performance. The fee is deducted from the fund’s assets before returns are reported, so you pay it in up years, down years, and flat years. This is why fee drag compounds so significantly over long periods.

No. The Canadian Securities Administrators banned the sale of new DSC mutual funds in June 2022. However, investors who purchased DSC funds before the ban may still have active redemption schedules with early withdrawal penalties. Check your fund facts document or contact your advisor before switching existing DSC fund holdings.

Inside a TFSA or RRSP, transferring from mutual funds to ETFs has no tax consequences. Inside a non-registered account, selling a mutual fund that has appreciated triggers a capital gains event. Most advisors recommend prioritising the switch in registered accounts first, zero tax cost, immediate and permanent fee reduction.