Asset Allocation Strategy Explained: How to Build a Simple ETF Portfolio

Introduction

Most people start investing by asking the wrong question.

They ask: “Which ETF should I buy?”

The better question, the one that actually shapes your long-term outcome, is: “How should I divide my money between different types of investments?”

That’s asset allocation. And it’s probably the most important investment decision you’ll make.

I know that sounds like an exaggeration. But research consistently shows that asset allocation, i.e., how you split your portfolio between stocks, bonds, and other assets, explains more of your long-term returns than any individual fund you pick.

This guide breaks it down simply. No jargon. No predictions. Just a clear explanation of what asset allocation strategy means, what simple ETF portfolios look like in practice, and why keeping it straightforward usually wins.

What Is Asset Allocation? (And Why It Matters More Than Stock Picking)

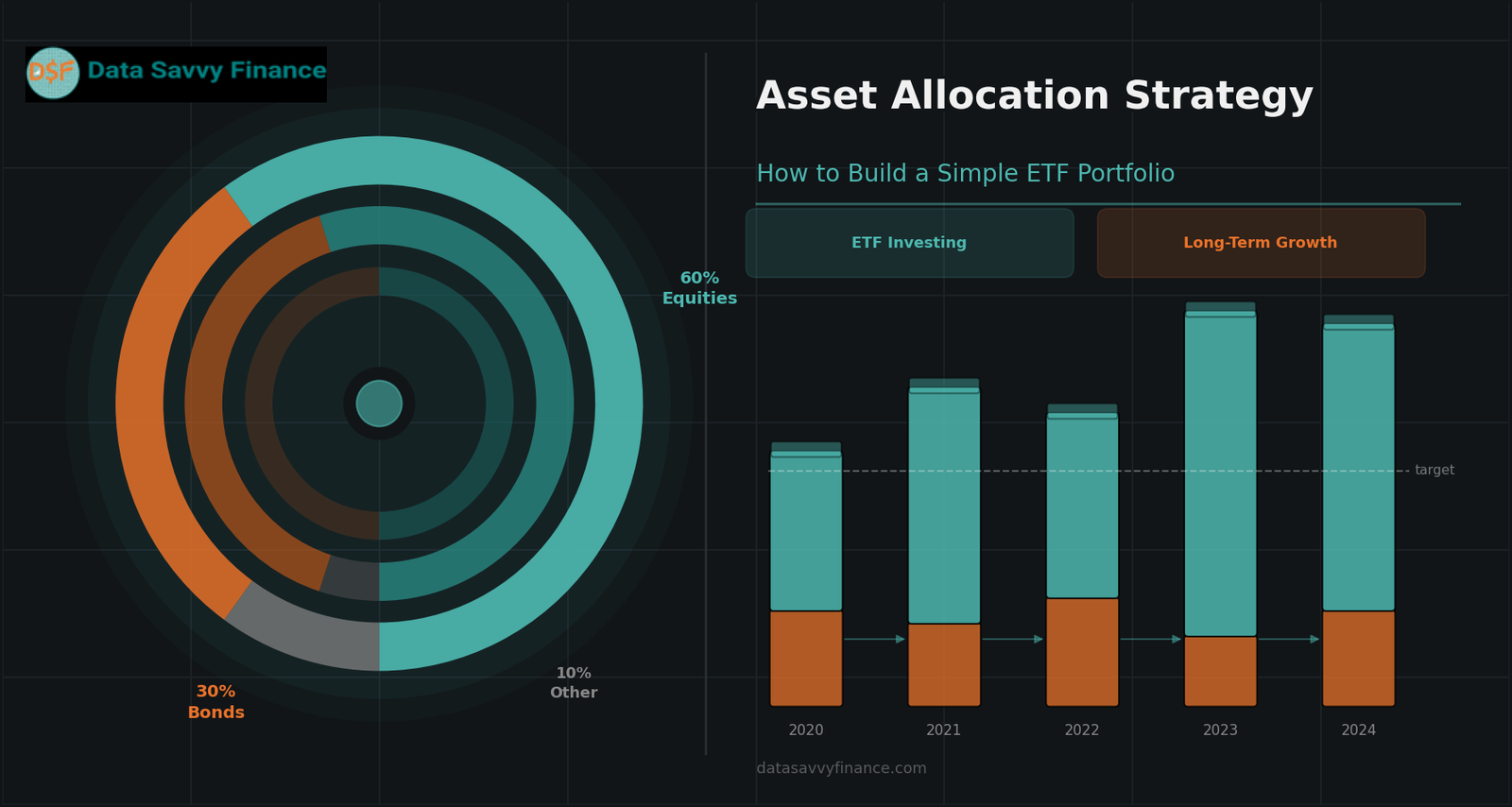

Asset allocation is how you divide your investment portfolio between different asset classes — primarily stocks and bonds.

That’s it. Sounds simple, right? But this single decision has more impact on your long-term results than almost anything else you do as an investor.

Here’s why. Stocks and bonds behave differently:

Stocks tend to grow faster over long periods, but they swing up and down dramatically in the short term.

Bonds grow more slowly, but they’re more stable, they often hold value (or even rise) when stocks are falling.

When you combine them, you get a portfolio that smooths out the ride without completely sacrificing growth. The ratio you choose, 80/20, 60/40, or something else, reflects how much volatility you’re willing to sit with while your investments grow.

This is what financial educators mean when they talk about risk tolerance. It’s not about how brave you are. It’s about how much your portfolio can drop in a bad year without causing you to panic-sell at the worst possible time.

Key takeaway: Asset allocation defines your risk profile. Getting this right matters more than which specific ETF you pick inside each asset class.

How ETFs Make Asset Allocation Simple

Before ETFs existed, building a diversified portfolio meant buying dozens of individual stocks and bonds. It was expensive, complicated, and out of reach for most regular investors.

ETFs changed that completely.

A single ETF can hold hundreds, sometimes thousands, of individual securities. Buy one stock ETF and you own a small piece of hundreds of companies at once. That’s diversification that would have cost a fortune to replicate on your own just 30 years ago.

For asset allocation purposes, you really only need a few building blocks:

A broad stock ETF (Canadian, US, or global equities) for growth

A bond ETF for stability and income

Optionally, an international ETF for broader geographic diversification

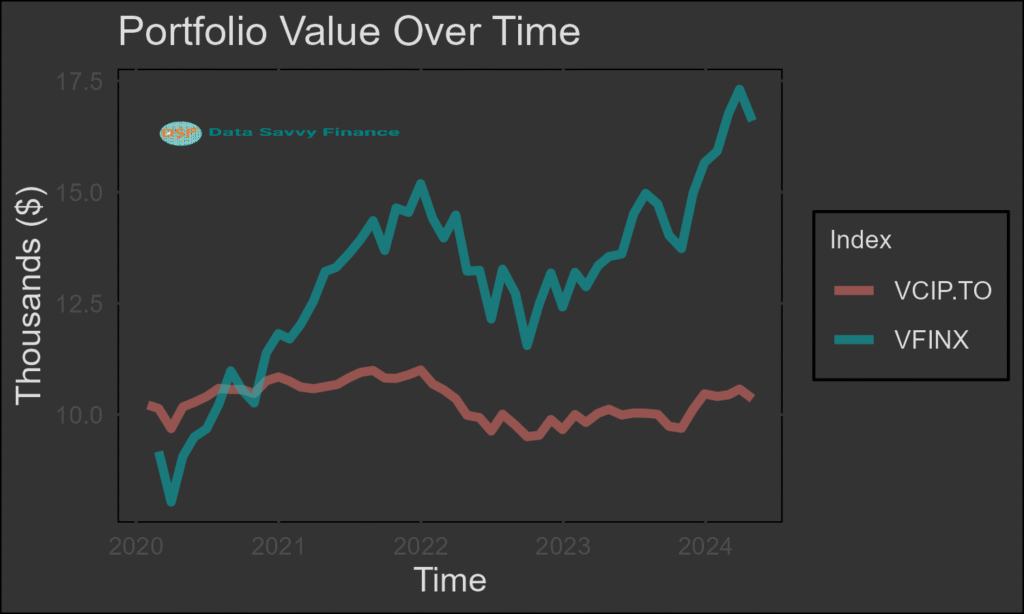

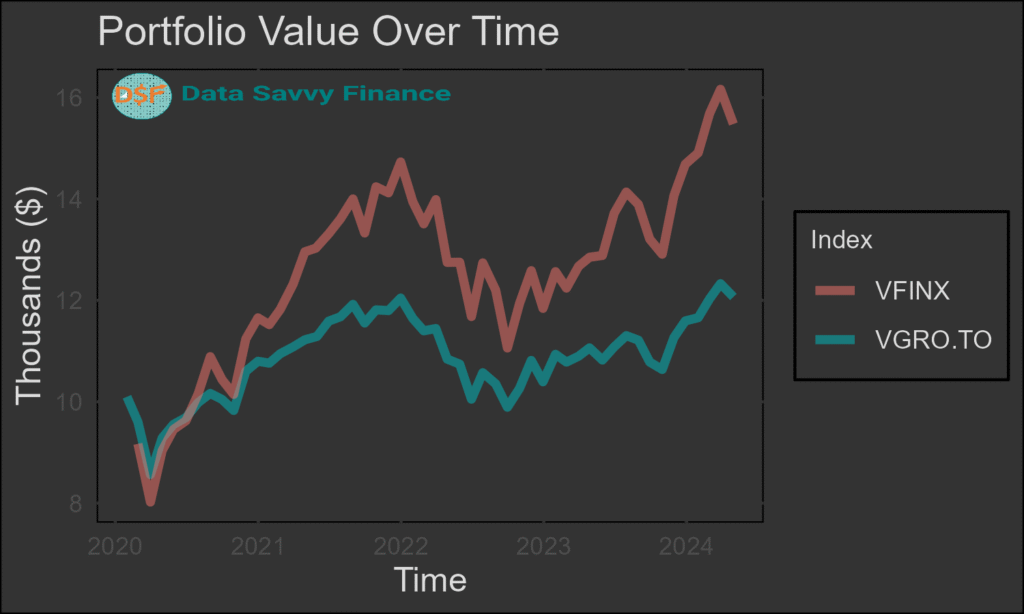

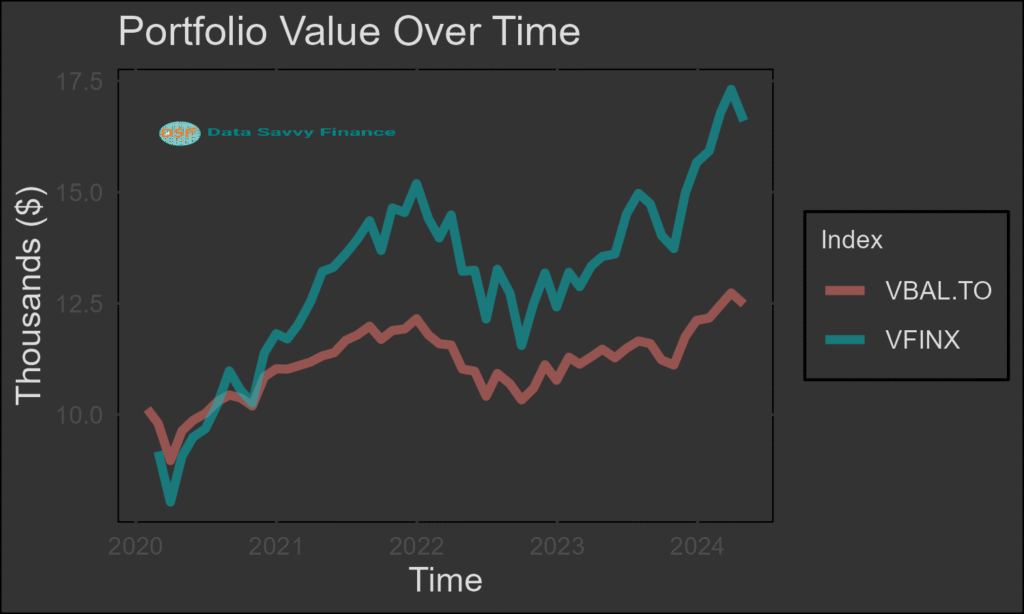

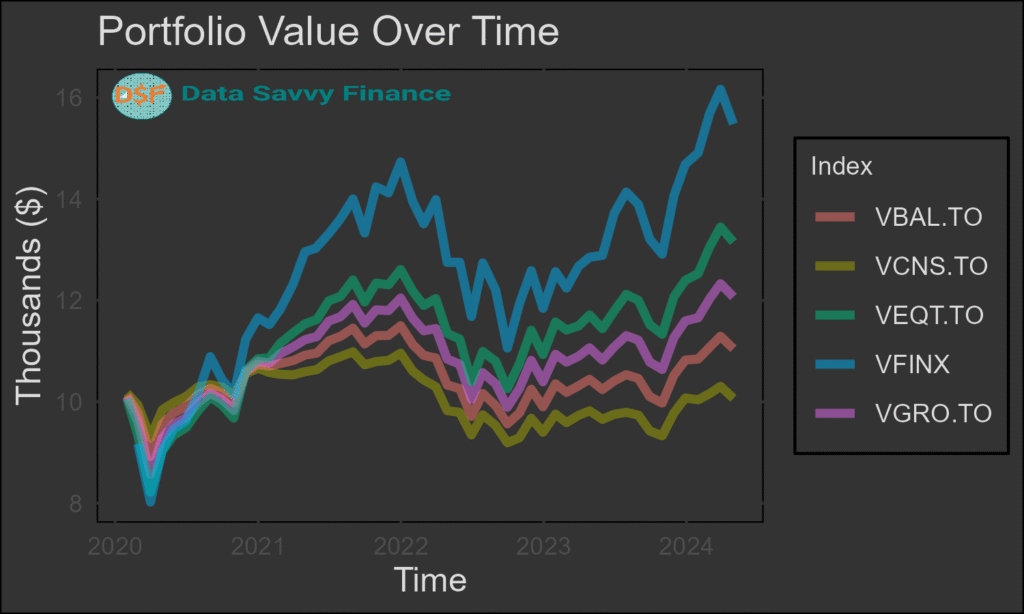

That’s it. Three ETFs can build a complete, well-diversified portfolio. This is sometimes called the “three-fund portfolio” approach, and it’s the foundation of most evidence-based investing strategies today.

In Canada, some popular all-in-one ETFs like VGRO, XBAL, or VCNS take this even further, they bundle the whole allocation into a single fund that automatically rebalances itself. For true beginners, these are worth knowing about.

On management expense ratios: Keep MER in mind when selecting ETFs. A stock ETF charging 0.03% and one charging 1.5% can produce dramatically different outcomes over 25 years, even if they track the same index. See how fees impact your portfolio using this investment growth calculator.

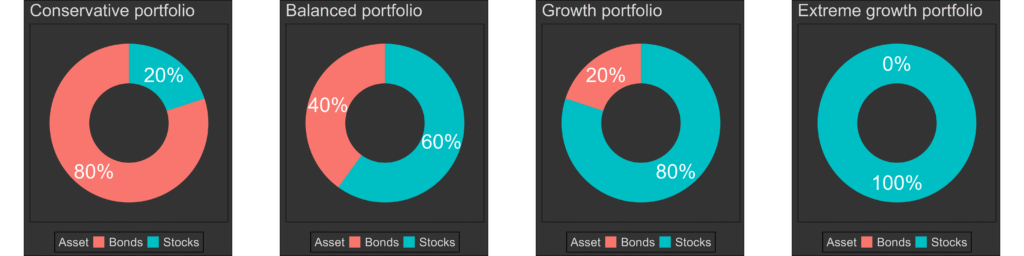

Simple ETF Portfolio Examples (Conservative, Balanced, Growth)

There’s no “correct” asset allocation. The right mix depends entirely on your situation, specifically how long you plan to invest and how comfortable you are with short-term losses.

Here are three straightforward starting points:

Conservative (lower risk)

~30–40% stock ETFs

~60–70% bond ETFs

Lower expected growth, but smoother year-to-year performance

Best for shorter time horizons (under 10 years) or investors close to retirement

Balanced (moderate risk)

~50–60% stock ETFs

~40–50% bond ETFs

Middle ground between growth and stability

A common starting point for investors in their 40s and 50s

Growth (higher risk)

~80–100% stock ETFs

~0–20% bond ETFs

Higher long-term growth potential, but expect significant short-term swings

Best suited for investors with 20+ year horizons who won’t panic during market drops

One important reality check: there is no allocation that avoids all risk. Even a conservative portfolio will lose value during a serious market downturn. The goal isn’t to eliminate volatility, it’s to match your allocation to a level of volatility you can actually live with without abandoning your plan.

Why Simple ETF Portfolios Often Beat Complex Ones

It feels like a more sophisticated strategy should produce better results. More funds, more diversity, more fine-tuning, surely that adds up to more performance?

In practice, the opposite is usually true.

Simple ETF portfolios have several structural advantages that complex ones don’t:

Lower costs. Every additional fund adds its own fee drag. A portfolio of 3–4 low-cost ETFs will almost always have a lower blended MER than one with 10+ actively managed positions.

Fewer behavioral mistakes. The more moving parts you have, the more opportunities there are to second-guess yourself. Investors with simple portfolios make fewer changes, and staying invested, not reacting to noise, is one of the biggest drivers of long-term returns.

Easier rebalancing. With 3 funds, rebalancing takes 20 minutes once a year. With 15 funds, it becomes a project, and projects get postponed.

Less cognitive load. This one gets underestimated. When your portfolio is easy to understand, you’re more likely to actually understand it. That means less anxiety, fewer panicked decisions during market drops, and better outcomes over time.

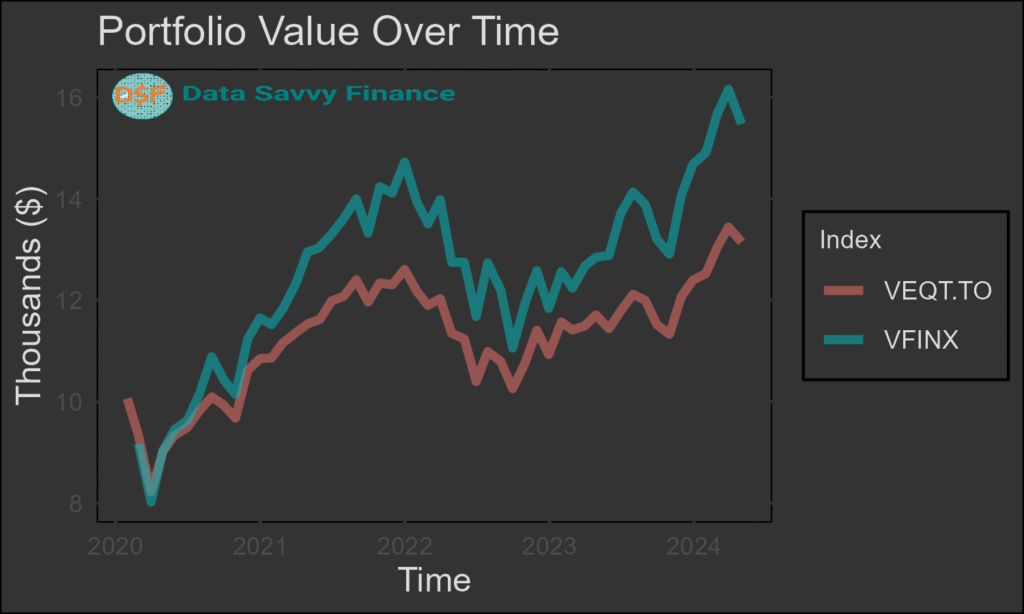

The research bears this out: passive, low-cost, simple portfolios outperform the majority of actively managed strategies over 10+ year periods, net of fees.

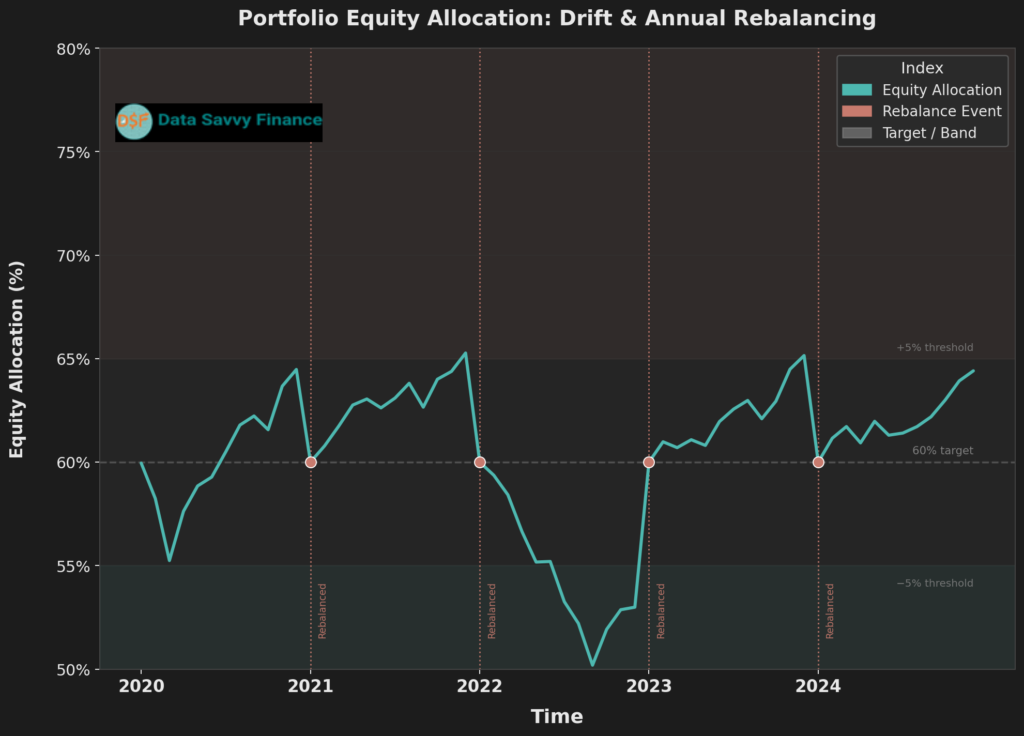

What Is Rebalancing and Why Does It Matter?

Let’s say you set up a 70% stocks / 30% bonds portfolio. After a strong year in the stock market, stocks have grown and now represent 82% of your portfolio. Your original allocation has drifted.

Rebalancing means bringing it back to 70/30.

You do this by selling some of the asset class that grew and buying more of the one that lagged. It sounds counterintuitive, selling the winner, buying the laggard, but it enforces a discipline that most investors struggle with on their own: buy low, sell high.

More importantly, rebalancing keeps your risk profile where you intended it to be. Without it, a growth-oriented market run can silently push a balanced investor into a growth investor’s risk exposure, which only becomes obvious when the next market correction hits.

How often should you rebalance?

Once per year is a reasonable rule of thumb for most long-term investors. Some use a threshold approach instead, rebalancing whenever any asset class drifts more than 5–10% from its target. Either works.

The key is consistency, not precision.

Asset Allocation and the Best Long-Term Investments

The phrase “best long-term investments” gets thrown around a lot in finance content. Most of the time it refers to individual stocks, sectors, or trends that someone thinks will outperform.

But the evidence points somewhere less exciting, and more reliable.

The best long-term investments for most people share three characteristics:

They’re diversified. No single company, sector, or country can sink the whole portfolio.

They’re low cost. Fees are the only guaranteed drag on returns. Minimizing them is the one lever every investor fully controls.

They’re aligned with your actual risk tolerance. The “best” allocation is the one you’ll hold through a 30% market drop without selling.

A well-constructed simple ETF portfolio, a broad stock ETF, a bond ETF, calibrated to your time horizon, satisfies all three conditions. It’s not glamorous. But it’s what actually works for the vast majority of long-term investors.

Asset Allocation by Age, A Starting Framework

Your ideal allocation isn’t static. As you approach retirement, the stakes change. A major market drop at 35 gives you decades to recover. The same drop at 63, one year before you plan to start withdrawing, hits very differently.

A common rule of thumb: subtract your age from 110 to get your stock allocation.

Age 30 → ~80% stocks, 20% bonds

Age 45 → ~65% stocks, 35% bonds

Age 60 → ~50% stocks, 50% bonds

This is a rough framework, not a prescription. Someone at 60 who is still working, has a defined pension, and won’t touch their TFSA for 15 years might reasonably hold 70% stocks. Someone at 40 who is extremely risk-averse or has a 5-year horizon might prefer 50/50.

The point is that your allocation should evolve over time, and a periodic review (once a year is plenty) should include a check on whether your current mix still fits your situation.

Canadian Context: ETF Asset Allocation in an RRSP or TFSA

Canadian investors have a structural advantage that often goes underappreciated: the ability to hold low-cost ETFs inside registered accounts like an RRSP or TFSA, sheltering growth and income from tax.

For most DIY investors in Canada, the setup looks something like this:

- Open a self-directed brokerage account (Questrade and Wealthsimple Trade are popular options for low-cost ETF investing)

- Choose a target allocation based on your time horizon and risk tolerance

- Select 2–4 low-cost ETFs (or a single all-in-one like XGRO, VGRO, or ZBAL)

- Set up automatic contributions

- Rebalance annually

The MER on Canadian all-in-one ETFs typically runs between 0.18% and 0.25%, a fraction of what most mutual funds charge. That difference compounds significantly over a 25-year RRSP horizon.

Want to see exactly how much that fee gap costs over time? Use this investment growth calculator to run the numbers.

Conclusion

Asset allocation strategy is not exciting. It doesn’t come with tips, predictions, or a hot ticker symbol. But it is, by almost every measure, the most important structural decision you make as a long-term investor.

A simple ETF portfolio, calibrated to your actual risk tolerance, low in fees, and rebalanced once a year, gives you exposure to long-term market growth without the complexity that causes most investors to make costly mistakes.

The goal isn’t to build the perfect portfolio. It’s to build one you’ll actually stick with.

Start simple. Keep costs low. Rebalance when you drift. And let time do the compounding.

FAQ Asset Allocation Strategy

Asset allocation strategy is how you divide your portfolio between different asset classes — primarily stocks and bonds. It’s the single biggest factor influencing your portfolio’s long-term risk and return profile.

A simple ETF portfolio for beginners typically consists of 2–3 ETFs: a broad stock ETF for growth, a bond ETF for stability, and optionally an international stock ETF for geographic diversification. In Canada, all-in-one ETFs like XGRO or VBAL combine these into a single fund.

Once per year is a good rule of thumb for most long-term investors. Some prefer threshold-based rebalancing, adjusting when any allocation drifts more than 5–10% from its target.

A common guideline is to subtract your age from 110 to get your approximate stock allocation. At 30, that’s roughly 80% stocks and 20% bonds. At 60, roughly 50/50. This is a framework, not a rule, your income stability, time horizon, and risk tolerance all matter.

Yes. Decades of academic research and real-world performance data show that low-cost, diversified ETF portfolios outperform the majority of actively managed strategies over 10+ year periods, primarily because of lower fees and fewer behavioral mistakes.

Conservative portfolios hold mostly bonds (60–70%), offer lower growth but less volatility. Balanced portfolios split roughly 50/50 between stocks and bonds. Growth portfolios hold mostly stocks (80–100%) for higher long-term returns with more short-term swings.