How a Questrade TFSA Works: $102,000 in Tax-Free Room, $0 ETF Commissions, 15-Minute Setup (2026)

If your TFSA is sitting in cash or a bank mutual fund charging 2% a year, you may be giving up tens of thousands in long-term returns you can’t see on your statement. This guide explains how a Questrade TFSA works, what the contribution limits are, what setup looks like, and how commission-free ETF investing inside a TFSA differs from what most Canadians are doing right now.

Educational disclaimer This article describes how a TFSA account functions at Questrade for educational purposes only. It does not constitute financial, investment, or tax advice and does not recommend opening an account with any specific institution. Every investor’s situation is different. Consult a registered financial advisor before making investment decisions.

How a Questrade TFSA Works: $102,000 in Tax-Free Room, $0 ETF Commissions, 15-Minute Setup (2026)

Here is something that surprised me when I first looked into this properly. Over 40% of Canadians who have a TFSA are holding it entirely in cash. Not invested. Just sitting there earning maybe 1% while inflation chips away at the real value, year after year. I was one of those people for a while, and honestly, nobody told me there was a different way to use the account.

A TFSA is not a savings account. The name is misleading. It is a registered account that shelters whatever is inside it from tax. The investments grow tax-free. Withdrawals are tax-free. The government does not touch any of it. What you put inside the account, whether that is ETFs, GICs, stocks, or cash, determines how your money actually grows. The account type is just the container.

This guide explains how a TFSA held at Questrade works, what the contribution limits look like in 2026, what the account setup process involves, and how the cost structure compares to holding a TFSA at a typical bank. It is educational. It is not a recommendation to open any account anywhere.

What Is a TFSA and How Does It Actually Work

A lot of people know the acronym. Fewer people know what it actually means for how their money grows.

The Tax-Free Savings Account was introduced by the federal government in 2009. Every Canadian resident aged 18 or older accumulates contribution room each year. Any investment growth inside the account is sheltered from tax entirely. You do not pay capital gains tax when your ETFs go up. You do not pay income tax when you withdraw. The money comes out exactly as it grew, with no CRA involvement on the way in or out.

Compare that to a non-registered account. In a non-registered account, every dollar of capital gain, every dividend, every interest payment is taxable income. The TFSA eliminates that friction entirely for whatever fits inside it.

The part most people miss is this: the TFSA is not limited to savings products. It can hold almost any investment eligible for registered accounts in Canada. That includes individual stocks, bonds, GICs, and ETFs. When you hold a low-cost index ETF inside a TFSA, you are combining tax-free compounding with low fees. Those two things together are among the most powerful advantages available to a Canadian investor who does not want to pay for managed advice.

How Much TFSA Contribution Room Is Available in 2026

This is the part that makes a lot of newcomers nervous. Contribution limits, cumulative room, over-contribution penalties. It sounds complicated. It is actually pretty straightforward once you see the numbers.

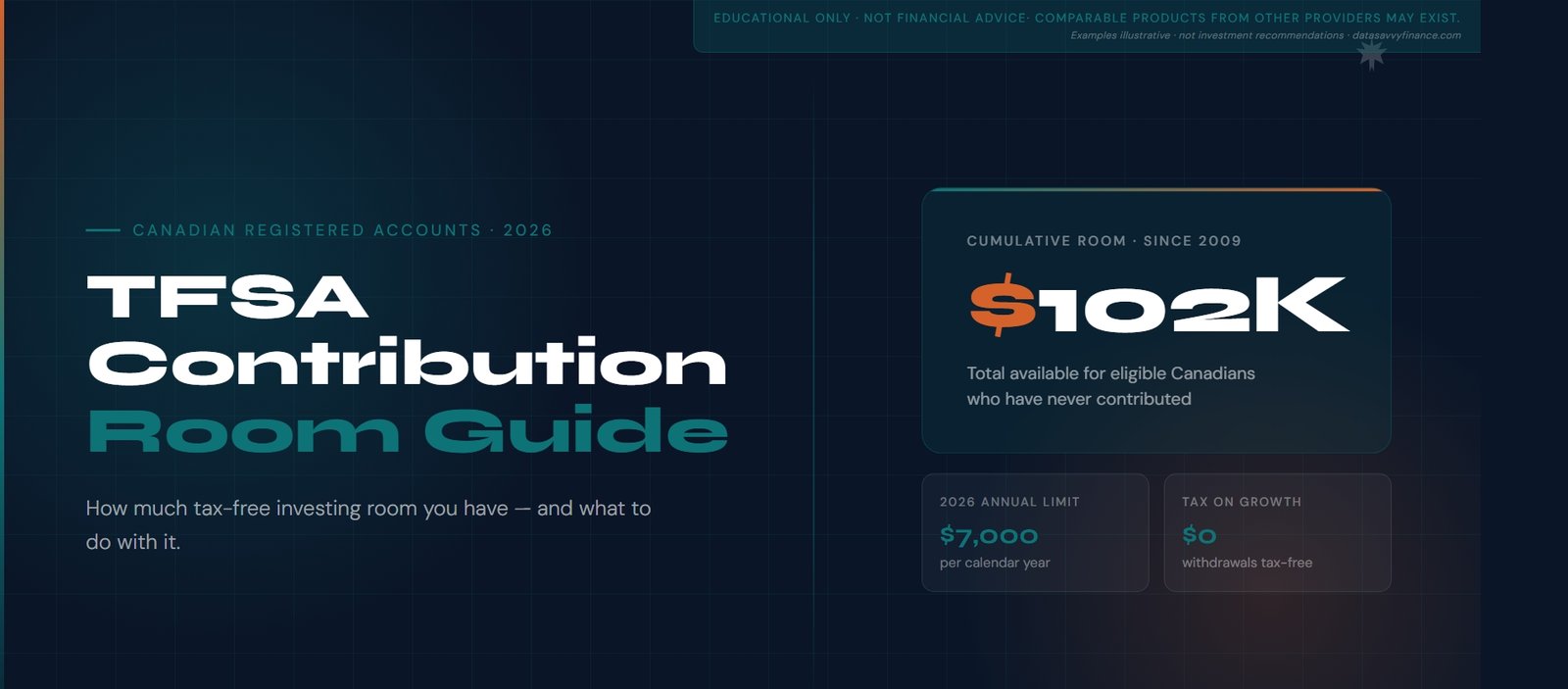

The annual TFSA contribution limit has been $7,000 per year for 2024 and 2025. The 2026 limit is expected to remain at $7,000, though this is indexed to inflation and adjusted in $500 increments, so confirm the current figure on the CRA website before contributing.

What matters more for most investors is the cumulative room. TFSA contribution room has been accumulating since 2009 for eligible Canadians. If you were 18 or older in 2009 and have never contributed, your total available room as of 2026 is $102,000. That is a significant amount of tax-sheltered investing space that many Canadians are leaving unused.

A few rules worth understanding before you deposit anything.

The over-contribution penalty is 1% per month on any excess amount. CRA enforces this. It adds up quickly and the agency does track it. Do not guess at your available room.

The most reliable way to check your contribution room is to log into CRA My Account at canada.ca. One caveat: CRA’s figures are always one year behind. They will not reflect contributions you have already made in the current calendar year. You need to subtract those yourself. A simple running total in a notes app or spreadsheet is enough.

If you withdraw from your TFSA, that contribution room does not come back until January 1st of the following year. Re-contributing too soon in the same year is one of the most common ways investors accidentally go over their limit.

How the Questrade TFSA Fee Structure Compares to a Bank

This is where the practical difference becomes clear, and where the math matters most.

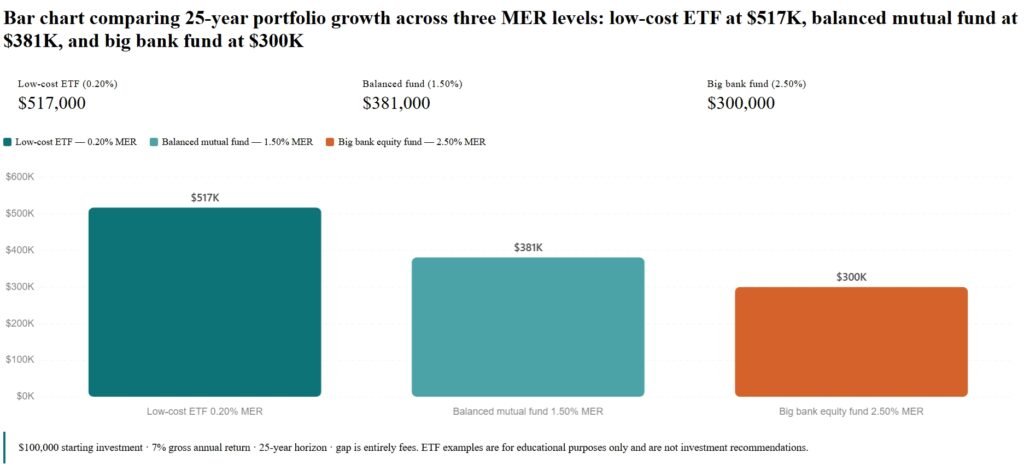

Most Canadians who hold a TFSA at one of the big banks are holding it in either cash savings products or bank-branded mutual funds. The management expense ratios on Canadian bank mutual funds typically range between 1.5% and 2.5% per year. That fee is deducted from the fund’s returns automatically. It does not show up as a line item on your statement. It is invisible unless you go looking for it.

At Questrade, a self-directed TFSA has no monthly platform fee and no commission on ETF purchases. Selling ETFs costs $4.95 to $9.95 per trade. The ETFs available, including all-in-one index funds like XEQT or XBAL, carry MERs in the range of 0.10% to 0.20% per year.

The fee difference between a 2% mutual fund MER and a 0.20% ETF MER is 1.8 percentage points annually. On a $100,000 portfolio held for 25 years, that gap compounds into a difference worth well over $150,000 in final portfolio value, depending on return assumptions. The investment growth calculator on DatasavvyFinance.com allows you to model this with your own numbers and time horizon.

ETF examples are provided for educational purposes only and are not investment recommendations. Comparable products from other providers may exist.

Starting with $100,000 and assuming 7% gross annual return over 25 years. The $217,000 gap between the low-cost ETF and the big bank fund is entirely the result of fee differences, no difference in strategy or market returns. For educational purposes only.

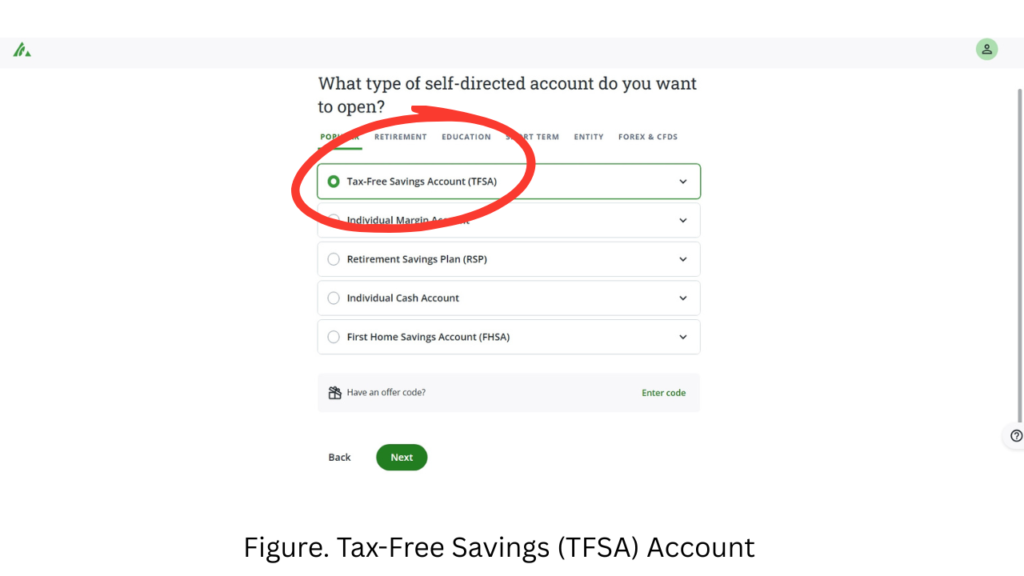

What the Questrade TFSA Setup Process Involves

The account application process at Questrade is straightforward. Here is what it involves, based on how the process currently works.

What you need before starting:

- Social Insurance Number (SIN)

- Government-issued photo ID (driver’s licence or passport)

- Canadian residential address (P.O. box not accepted)

- Canadian bank account for funding

- No minimum deposit is required for a self-directed account

How the process works:

The online application asks for personal information, your SIN, residential address, and employment details. Questrade also asks about investing experience and risk tolerance as part of the account profile. These answers determine your account settings, not approval.

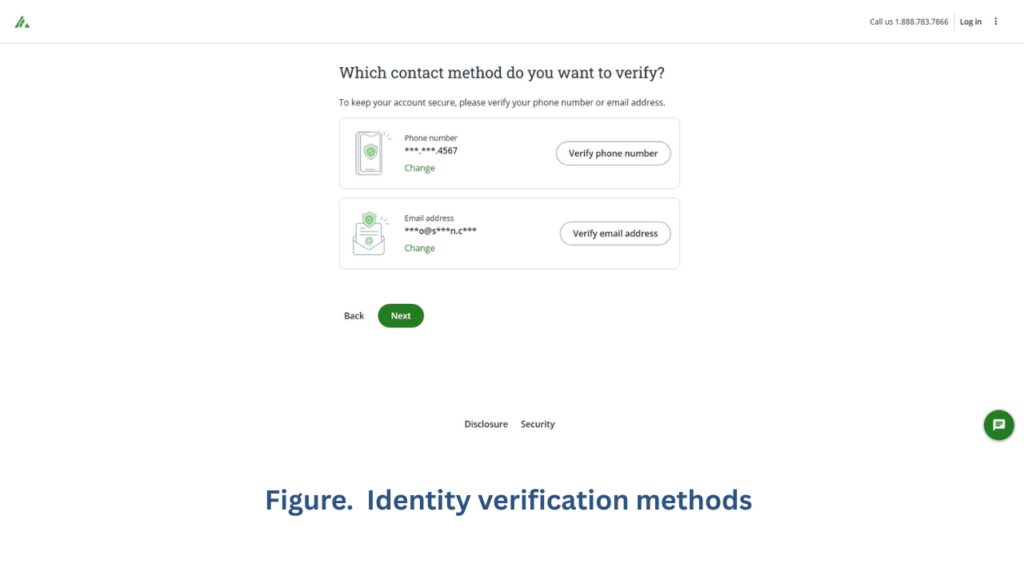

Identity verification involves uploading a photo of your government-issued ID. This step is reviewed during business hours and typically clears within one to two business days. A clear, well-lit photo avoids the most common delay.

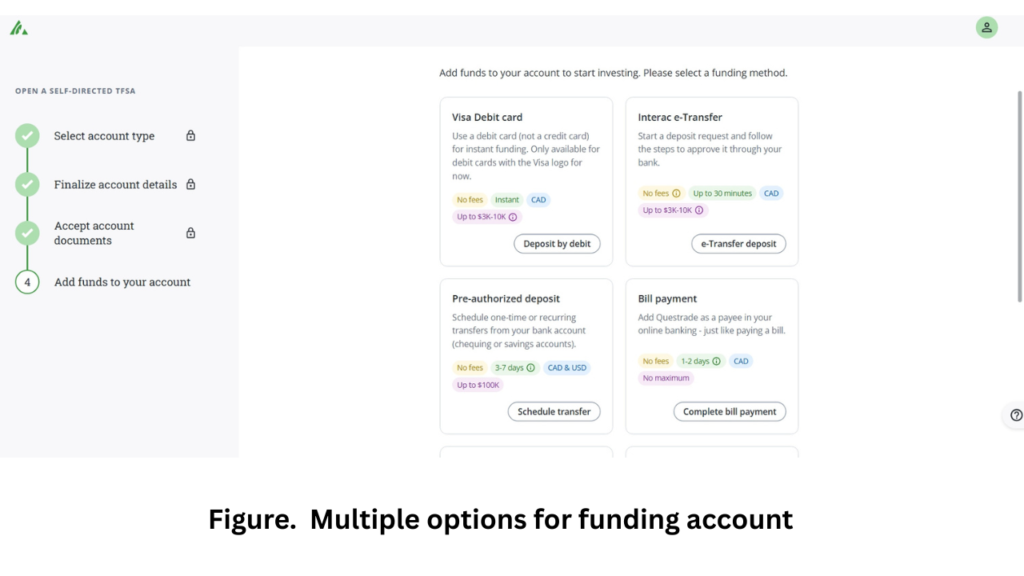

Funding the account is most commonly done through bill payment via online banking. You add Questrade as a payee and use your Questrade client ID as the account number. Bill payment transfers typically take two to three business days to settle before funds are available to trade.

From start to first trade, most people complete the process within one week. The application itself takes roughly 10 to 15 minutes.

A note on account types: Questrade offers both a self-directed TFSA, where you choose your own investments, and Questwealth Portfolios, a managed option that requires a $250 minimum deposit and charges an annual management fee. These are different products with different cost structures.

TFSA vs RRSP: How to Think About the Difference

This question comes up constantly for anyone opening their first registered account, and it is worth addressing directly.

A TFSA and an RRSP are both tax-advantaged registered accounts available to Canadians, but they work differently.

A TFSA uses after-tax dollars. You contribute money you have already paid income tax on. The growth inside the account is tax-free, and withdrawals do not count as income. Contribution room is not income-dependent, every eligible Canadian gets the same annual amount regardless of how much they earn.

An RRSP uses pre-tax dollars. Contributions generate a tax deduction in the year they are made, which reduces your taxable income. The investments grow tax-deferred, not tax-free. When you withdraw, the amount is taxed as income in that year.

The practical difference for most beginners: if your current income is low to moderate, the immediate tax deduction from an RRSP is less valuable than it will be when your income is higher. The TFSA’s flexibility, no tax on withdrawals, room returned the following year after withdrawals, no income requirement, makes it the simpler starting point for most early-career investors.

Both accounts can hold the same types of investments. Both can be held at the same brokerage under a single login. The choice between them is about tax timing and personal income trajectory, not about which account is universally better. This article describes one common approach to thinking about the decision, not a recommendation for any specific investor.

Common TFSA Mistakes Worth Knowing About

A few situations come up repeatedly and are worth understanding before you contribute anything.

Over-contributing. The 1% monthly penalty is real. CRA figures lag by one year, so any contributions made in the current calendar year need to be tracked manually. Subtracting those from the CRA figure before depositing is the only reliable approach.

Withdrawing and re-contributing in the same calendar year. This is the most common accidental over-contribution. If you withdraw $10,000 from your TFSA in March, that $10,000 of room does not return until January 1st of the following year. Depositing it back before then puts you over your limit.

Treating the TFSA as a cash account. An account sitting entirely in cash is earning a fraction of what a diversified ETF portfolio might return over a long time horizon. The tax shelter only works if there is something inside the account that can grow. This is an observation about how the account functions, not advice about what to do with yours.

High-fee funds inside the account. The tax-free shelter amplifies both gains and the drag from fees. A mutual fund charging 2% inside a TFSA is losing the same 2% annually as it would outside one. The fee does not disappear because the account is registered.

A few things worth thinking about

Asset allocation. Before choosing any ETF, understanding how much risk you are comfortable with over a long time horizon gives every subsequent decision more clarity. Growth-oriented, balanced, or conservative allocations are all different in practice, and the right answer is personal. The ETF asset allocation guide on DatasavvyFinance.com explains the structural differences.

Regular contributions. The compounding math on a TFSA works best when contributions happen consistently over time. Even modest monthly amounts, say $100 to $200, compound differently over 25 years than the same total contributed as a lump sum later. The investment growth calculator lets you model different contribution schedules against each other.

MER impact over time. The fee difference between a low-cost ETF and a higher-MER fund compounds in the opposite direction from returns. A detailed breakdown of how MER compounds over a 25-year period shows the real numbers on this.

Conclusion

A TFSA at a low-cost brokerage platform represents one of the more efficient structures available for Canadian investors who want tax-free compounding at minimal ongoing cost. The contribution room, $102,000 cumulative as of 2026, is significant. The fee difference between what most bank-held TFSAs charge and what a self-directed ETF portfolio costs is real and compounds meaningfully over decades.

This article described how the account structure works, what the fee comparison looks like, and what the setup process involves. Whether a self-directed Questrade TFSA is the right structure for your specific situation depends on your income, goals, timeline, and existing accounts, none of which this article can assess.

For a comparison of how Questrade’s platform differs from Wealthsimple’s, the Questrade vs Wealthsimple guide covers the structural differences in detail.

Frequently Asked Questions

The online application takes approximately 10 to 15 minutes. Identity verification typically clears within one to two business days. Funding via bill payment takes an additional two to three business days to settle. Most investors are in a position to place their first trade within one week of starting the application.

No. Questrade does not require a minimum deposit for a self-directed account. The managed Questwealth Portfolios account has a $250 minimum. These are different products with different cost structures.

You need a Social Insurance Number (SIN), a Canadian residential address, and a government-issued photo ID such as a passport or driver’s licence. You must be a Canadian resident and at least 18 years old.

The 2026 annual TFSA contribution limit is $7,000. If you were 18 or older in 2009 and have never contributed, your cumulative available room as of 2026 is $102,000. Unused room carries forward automatically. Always verify your personal available room via CRA My Account at canada.ca before contributing, as CRA figures lag by one year and do not reflect contributions already made in the current calendar year.

The CRA charges 1% per month on any amount contributed over your available room. The penalty applies for every month the excess remains in the account. The most common cause is re-contributing a withdrawal in the same calendar year before the room is restored on January 1st.

Questrade does not charge monthly account fees on a self-directed TFSA. There are no trading commissions on ETF purchases. Selling ETFs and trading individual stocks do carry per-trade fees. For a buy-and-hold investor who purchases ETFs regularly and rarely sells, the ongoing platform cost is effectively zero beyond the ETF’s own MER.

Yes. Questrade allows Canadian and US-listed ETFs to be purchased inside a self-directed TFSA commission-free. Selling ETFs costs $4.95 to $9.95 per trade. ETF examples referenced on this site are for educational purposes only and are not investment recommendations.

A TFSA uses after-tax dollars. Growth is tax-free and withdrawals do not count as income. Contribution room is not income-dependent. An RRSP uses pre-tax dollars and provides a tax deduction in the contribution year, but withdrawals are taxed as income. Both can hold the same types of investments. Which account is more appropriate depends on individual income, tax circumstances, and goals, factors this article cannot assess for any individual investor.

Disclaimer

This content is for educational purposes only and does not constitute investment advice or a platform endorsement. The setup process and fee structure described reflect publicly available information about Questrade’s platform as of 2026 and may change. ETF examples are illustrative only and are not investment recommendations. Comparable products from other providers may exist.

Datasavvyfinance provides educational information only and does not provide financial, investment, legal, or tax advice. Content is not tailored to any individual. Investing involves risk, including loss of principal. Past performance does not guarantee future results. Consult a registered financial advisor before making investment decisions.