How a 1% MER Reduces a $100,000 Portfolio by $25,038 Over 10 Years, Modelled on Real Vanguard Data

Most investors know that fees matter. What most haven’t actually seen is the dollar number. I kept hearing “fees compound against you” for years before I finally sat down and ran the math myself, and honestly, the result was more concrete than I expected.

This analysis uses a decade of real Vanguard fund data, VOO at 0.03% MER and VFINX at 0.14% MER, from December 2014 to April 2024, to model how a 1% management expense ratio compounds against a $100,000 portfolio over 10 and 30 years. We also run three hypothetical MER scenarios to show the full range of what fee differences look like in dollar terms.

The short version: a 1% MER scenario costs $25,038 compared to the VOO baseline over the study period. That number does not include additional contributions. It is purely the compounding drag on a single $100,000 starting investment. The long version is below.

Educational disclaimer: ETF and mutual fund examples in this article are used to illustrate MER ranges for educational purposes only. They are not investment recommendations or endorsements. Comparable products from other providers exist across all categories listed above.

Introduction

This article goes into the actual math behind how MER compounds against investment returns over time. We use real fund data and run multiple fee scenarios side by side so the numbers are concrete, not theoretical. If you want the beginner-friendly explanation of what MER is and why it matters before getting into the data, start with the full guide on how MER impacts investment returns. To see how these fee savings apply inside a real Canadian registered account portfolio, the low-cost RRSP ETF portfolio article at DatasavvyFinance.com walks through a practical example at 0.175% total cost.

What does MER stand for in investing?

The Management Expense Ratio, or MER, is the annual fee charged by a mutual fund or ETF to cover its operating costs. It is expressed as a percentage of the fund’s average net assets. A fund with a 1% MER charges $1,000 per year on a $100,000 investment. That fee does not appear as a line item on your statement. It is deducted from the fund’s returns before the price is reported, which is why most investors do not notice it until they go looking.

MER applies to both mutual funds and ETFs, though the amounts differ significantly between the two. This article focuses on the compounding effect of that difference over time.

How is MER charged on ETF?

The Management Expense Ratio (MER) is calculated annually by investment funds to cover operating expenses, management fees, and administrative costs. MER is calculated as a percentage of the fund’s average net assets at an annual level. After calculations, the fund managers are deducing the MER amount from the fund’s returns. Managers often deduct the MER on a daily basis, by calculating the daily MER based on the annual MER. For example, daily MER = annual MER /252. They they deduce daily MER at the end of the day. This, in turn is reflected in the prices for the next day. ETFs usually have lower fees than mutual funds. However, these ETFs may be subject to other charges such as brokerage fees and commissions, as well as bid-ask spreads.

What MER ranges look like across fund types?

Mutual funds are typically higher MER than ETFs.

- Actively Managed ETFs: 0.3% to 1%

- Passively Managed ETFs: 0.03% to 0.5%

- Actively Managed Mutual Funds: 1% to 3%

- Index Mutual Funds: 0.1% to 1%

ETF and mutual fund examples in this article are used to illustrate MER ranges for educational purposes only. They are not investment recommendations or endorsements. Comparable products from other providers exist across all categories listed above.

While MER ranges is seeminlgy small its impact compounds over time, potentially reducing your overall investment returns significantly. MER has a reverse relationship between the compounding effect and the returns on the investment. That is, each year the investment value in the portfolio is decreased by the MER percentage. The longer the investment time horizon, the larger the compounding loss in the investment value becomes.

Even a difference of 0.5% in MER can lead to thousands of dollars in lost returns over decades. Higher MERs create a performance drag on your portfolio.

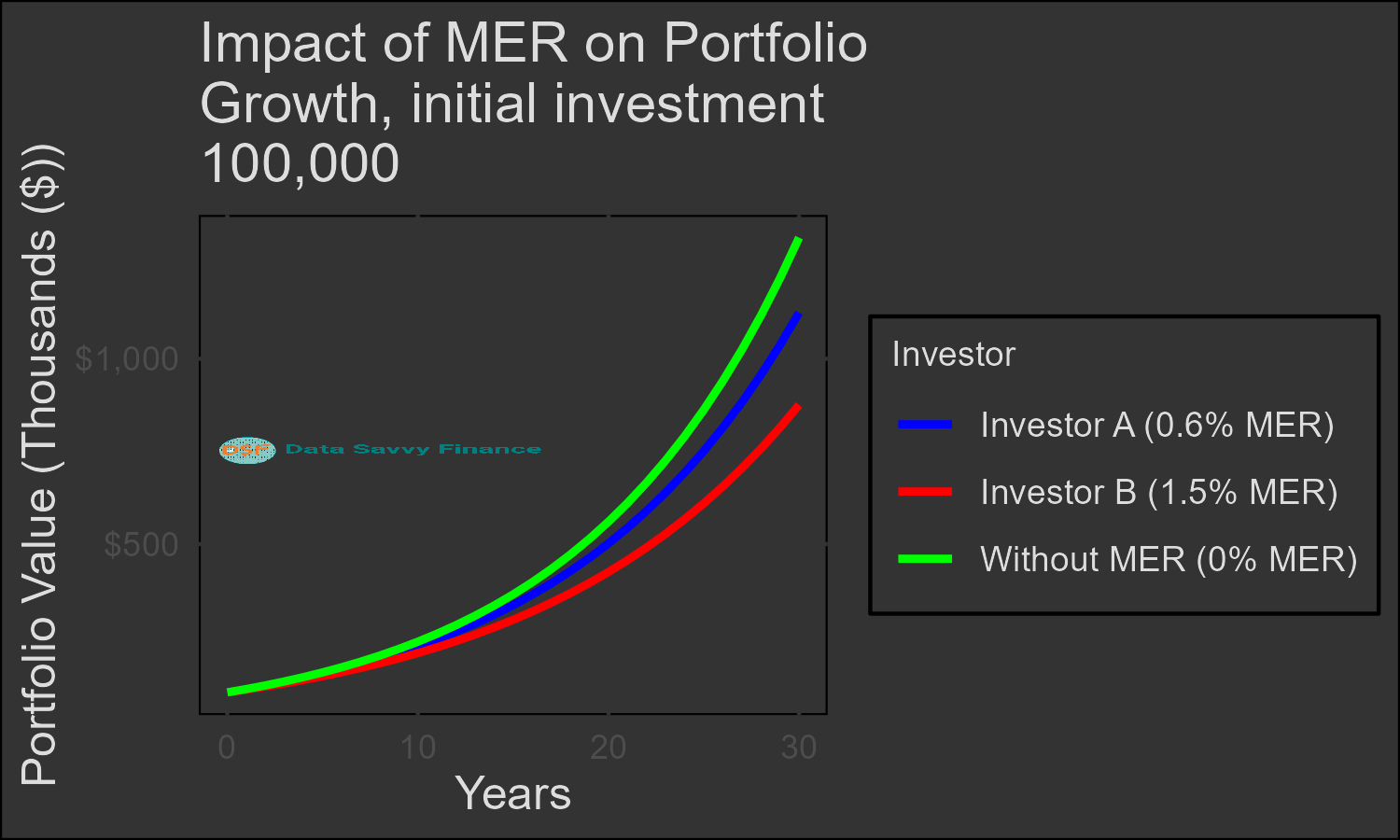

The Long-Term Impact of MERs

The long-term impact of lower MERs can be illustrated by the following hypothetical scenario:

Investor A chooses a fund with a 0.6% MER, while Investor B selects a similar fund with a 1.5% MER. Both invest $100,000 for 30 years, assuming 9% annual return before fees. Let’s assume now that returns and MER are constant over the investment time horizon of 30 years. Also, let’s assume that there is no additional investment contributions beyond the initial investment of $100,000. Then, after 30 years the returns will look like this:

- Investor A’s portfolio (0.6% MER): $1,124,290

- Investor B’s portfolio (1.5% MER): $875,495.5

- No MER portfolio (0% MER): $1,326,768

The difference of 1.1% in MER results in the following. Investor A having $248, 794.8 more in their portfolio over the 30 year investment time horizon!

Investment growth over the 30 year horizon is illustrated in the graph below:

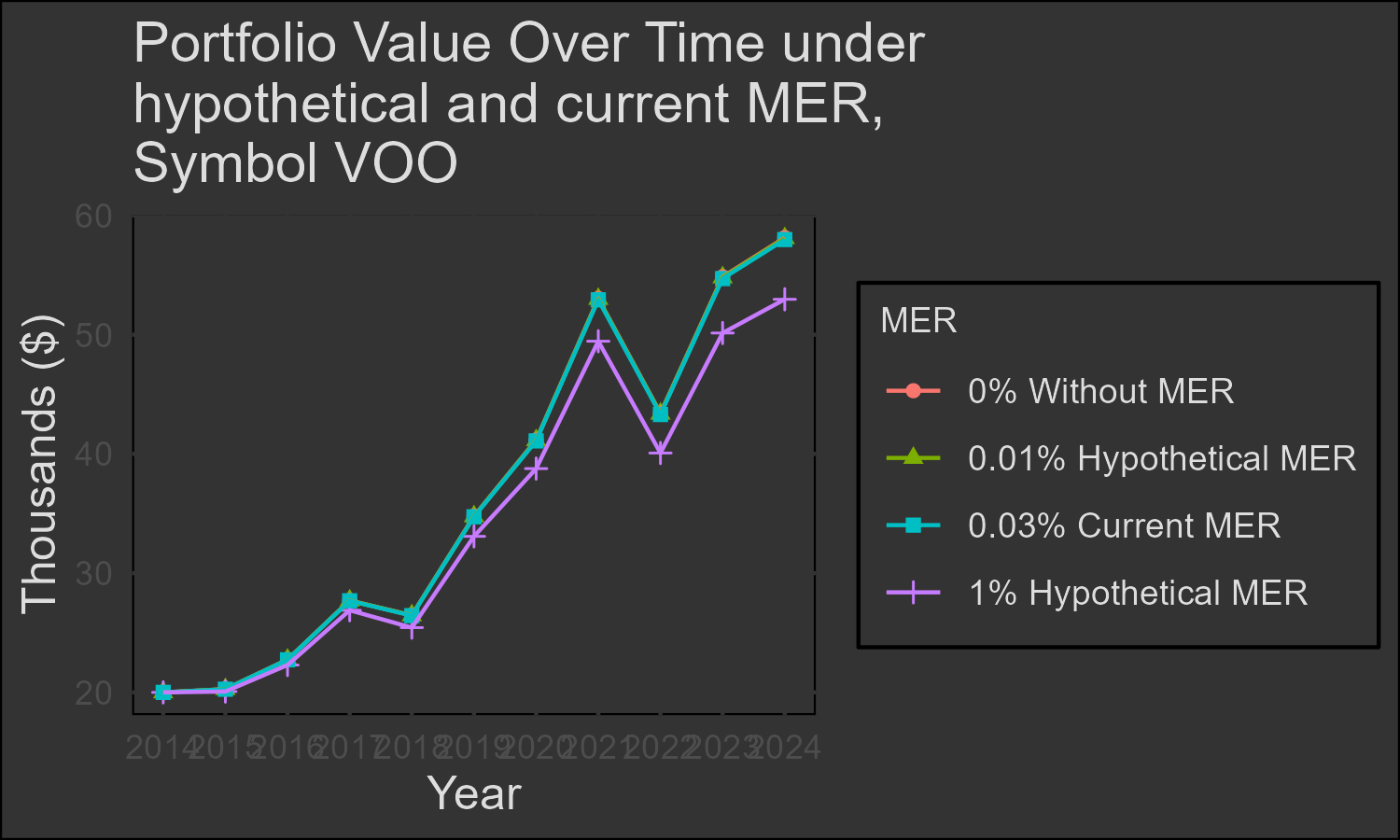

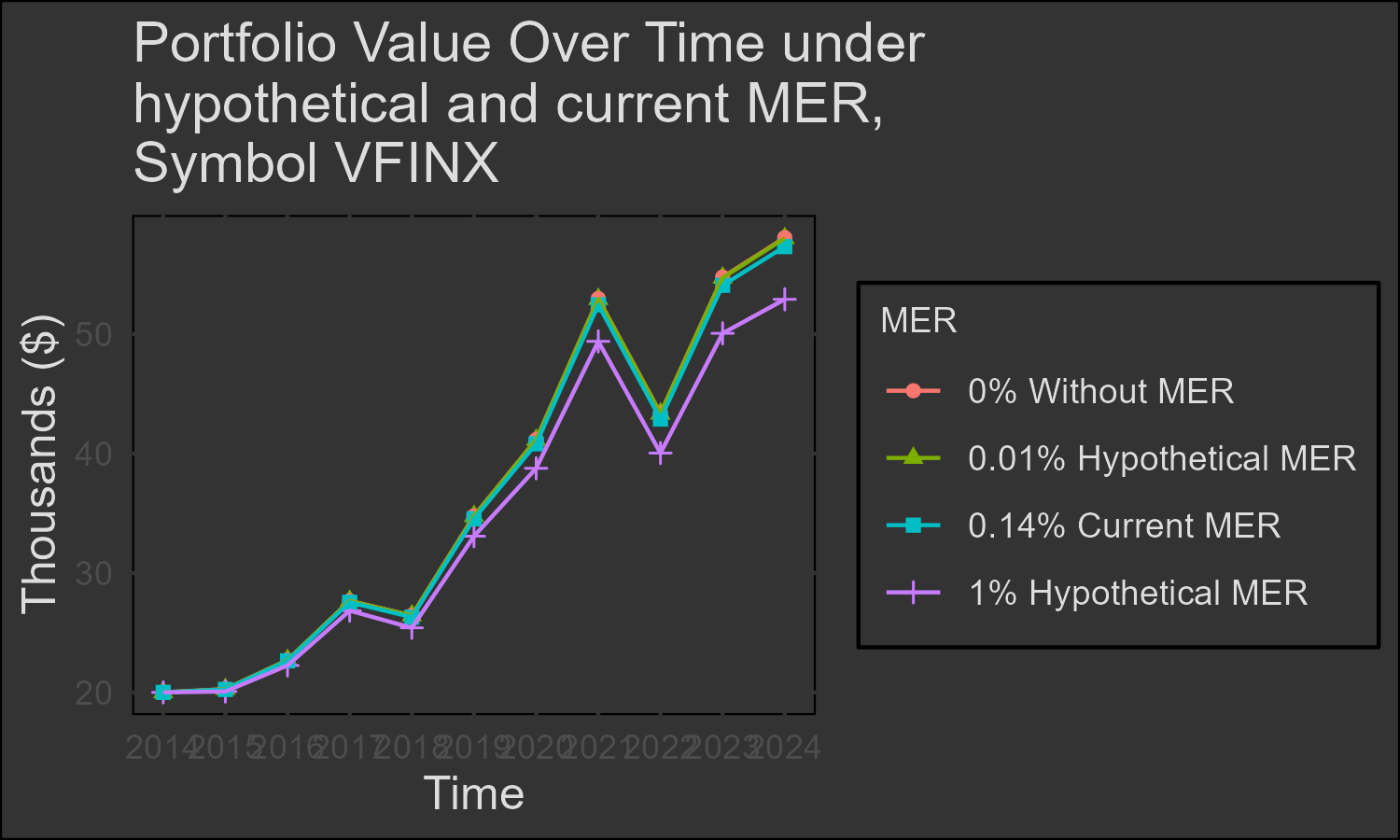

Case Study: Vanguard 500 Index Fund ETF Shares (VOO) ETF vs. Vanguard 500 Index Fund Investor Shares (VFINX)

Next, we will illustrate the impact of MER on portfolio growth. We’ll compare a Vanguard ETF VOO to an index mutual fund (VFINX) from December 2014 to April 2024. VOO ETF, which tracks the overall U.S. S&P 500 index, is known for its very low MER. MER was higher at 0.06% in 2010, and it gradually lowered to 0.03% in 2018 after which it is steady. VFINX, which is a passively managed index mutual fund that tracks the same US S&P 500 index, offers a comparison to VOO and demonstrates how MERs affect a large-cap focused index fund. The VFINX MER is 0.14% over the past 7 years, with an exception for the 2019, when the MER was 0.04%.

It is important to note that Vanguard index mutual funds such as VFINX, have much lower MERs than other mutual funds. Mutual funds require more administrative overhead, including managing shareholder accounts, sending out statements and handling customer service. VOO is an Exchange Traded Fund (ETF) usually held in self-directed brokerage accounts, which reduces the administrative burden on the fund holding company. VFINX is an “investor” share class which is accessible to smaller individual investors. Vanguard also offers “Admiral shares” investment funds for large investors, which has lower fee, similar to that of the ETFs like VOO.

Fee Structure in ETFs versus mutual funds

The lower fees of ETFs can be attributed to the ability of the ETFs to be traded during the day at market prices, offering more liquidity, and they are also more tax-efficient due to their creation/redemption process. In contrast, mutual funds are traded once per day at the Net Asset Value (NAV) which is calculated after the market closes. VFINX was formed in 1976, long before ETFs existed, and its higher price is partly due to this legacy. Despite the cost difference, both VFINX and VOO are designed to track the S&P 500 index. The slight difference in expense ratios doesn’t change their fundamental goal or strategy. VOO, with its lower expenses, may track the index slightly more closely over time, but both are considered highly efficient index-tracking instruments.

Assumptions in our simulation study

In our simulation study, we will assume that the expenses are constant over the entire period for better comparability between the hypothetical MER scenarios. VOO and VFINX have current MERs of 0.03% and 0.14%, respectively. We will use their current MERs to study the impact of the current MERs on their investment returns over an almost 20 year period. The hypothetical investment portfolio initial value is 100,000 (started in December 2014). We estimated the following metrics: portfolio end value at the end of the investment horizon (April 2024), Compound annualized growth (CAGR), annualized standard deviation, and Risk adjusted CAGR. We evaluated these metrics for VOO and VFINX under their current MERs, and under three other hypothetical MERs.

Let’s break down the performance under the studied MER scenarios:

- Current MER Portfolio (0.03% MER for VOO and 0.14% MER for VFINX). This represents the actual performance of VOO and VFINX with their existing, low MERs. VOO is known for its cost-efficiency, which contributes to its popularity among passive investors.

- No MER Portfolio. This hypothetical scenario shows how VOO and VFINX would perform if there were no management fees at all. While unrealistic, it serves as a benchmark to illustrate the drag that even minimal fees can have on long-term returns.

- 0.01% MER Portfolio. This ultra-low hypothetical MER scenario demonstrates how minimal fee impact returns compared to the current, no-fee and high-fee scenarios.

- 1% MER Portfolio. This higher hypothetical MER scenario, while still relatively low compared to many actively managed funds, shows a more pronounced impact on long-term returns.

Key Metrics

Different MER scenarios are compared for each VOO and VFINX:

- Portfolio End Balance Comparison: The difference in end portfolio values across these scenarios highlights the compounding effect of fees over two decades.

- CAGR (Compound Annual Growth Rate): Even small differences in MER can lead to noticeable differences in CAGR over long periods.

- Annual Standard Deviation: The MER doesn’t significantly affect the standard deviation, as it’s more related to the underlying assets’ performance.

- Risk-Adjusted CAGR: This metric helps investors understand the return relative to the risk taken, showing how fees impact efficiency.

Key Observations for VOO:

VOO has a very low MER of 0.03% that produces investment growth very comparable to the ultra low MER of 0.01% and No MER of 0%. The hypothesized high MER (1% MER) scenario will result in portfolio value that is lower by $ 25, 038.19 compared to the portfolio under the current VTI MER of 0.03%.

- The end balance portfolio value under the current MER portfolio (MER 0.03%) is lower than that of the hypothetical No MER (0% MER) portfolio by $ 810.99 over the two decades investment horizon.

- The end balance portfolio value under the current MER portfolio (MER 0.03%) is lower than that of the hypothetical low MER (0.01% MER) portfolio by roughly $ 540.4 over the two decades investment horizon.

- The end balance portfolio value under the current MER portfolio (MER 0.03%) is higher than that of the hypothetical High MER (1% MER) portfolio by $ 25, 038.19 over the two decades investment horizon.

The results are shown visually in the plot below as well as in the accompanying table.

Portfolio Performance

Metric

0.01% Hypothetical MER

1% Hypothetical MER

0% Without MER

0.03% Current MER

Start balance

100000.00

100000.00

100000.00

100000.00

End balance

290394.73

264816.12

290665.31

289854.31

AnnualizedReturn(CAGR)

10.25

9.31

10.26

10.23

St.Dev Monthly

4.34

4.34

4.34

4.34

St.Dev annually

15.05

15.05

15.05

15.05

Risk adjusted CAGR

8.71

7.91

8.72

8.69

Key Observations for VFINX:

VFINX has a low MER of 0.14% that produces investment growth very comparable to the ultra mow MER of 0.01% and No MER of 0%. The hypothesized high MER (1% MER) scenario will result in portfolio value that is lower by $ 22, 063.88 compared to the portfolio under the current VFINX MER of 0.14%.

- The end balance portfolio value under the current MER portfolio (MER 0.14%) is lower than that of the hypothetical No MER (0% MER) portfolio by $ 3,761.96 over the two decades investment horizon.

- The end balance portfolio value under the current MER portfolio (MER 0.14%) is lower than that of the hypothetical low MER (0.01% MER) portfolio by roughly $ 3, 491.62 over the two decades investment horizon.

- The end balance portfolio value under the current MER portfolio (MER 0.03%) is higher than that of the hypothetical High MER (1% MER) portfolio by $ 22, 063.88 over the two decades investment horizon.

The results are shown visually in the plot below as well as in the accompanying table.

Portfolio Performance

Metric

0.01% Hypothetical MER

1% Hypothetical MER

0% Without MER

0.14% Current MER

Start balance

100000.00

100000.00

100000.00

100000.00

End balance

290132.37

264576.87

290402.71

286640.75

AnnualizedReturn(CAGR)

10.24

9.29

10.25

10.11

St.Dev Monthly

4.36

4.36

4.36

4.36

St.Dev annually

15.09

15.09

15.09

15.09

Risk adjusted CAGR

8.69

7.89

8.70

8.59

Conclusion

The data from this study shows a consistent pattern: as MER increases, end portfolio value decreases, and that gap widens over longer time horizons. On a $100,000 starting investment using real Vanguard fund return data, the difference between a 0.03% MER and a hypothetical 1% MER compounds to $25,038 over the study period without any additional contributions.

This is not a dramatic result in isolation. But it illustrates a principle that scales with portfolio size and time. A $500,000 portfolio held for 25 years faces a proportionally larger compounding drag from a 1% fee difference than the numbers in this study reflect. The investment growth calculator on DatasavvyFinance.com allows you to model this with your own starting balance, contribution rate, and time horizon.

The study does not argue that any specific fund is the right choice for any investor. It models what fee differences look like in dollar terms using real return data. What an investor does with that information depends on their own goals, time horizon, and account structure — factors outside the scope of this analysis.

- The analysis allows investors to compare the performance of comparable large-cap index ETF (VOO) with a large-cap mutual index fund (VFINX) under various fee scenarios.

- It highlights the importance of considering the fee structure when making investment decisions.

- The comparison illustrates a structural difference in fee levels between index ETFs and traditional index mutual funds that has been observed consistently across comparable fund pairs. Individual investor circumstances vary and affect how relevant this difference is in practice.

- Note. It is important to acknowledge that for the illustration purposes the simulation example was simplified:

– The model uses a simplified annual MER deduction.

– The real world results might be slightly lower due the practice of daily MER fee deductions (before the NAV is calculated) which is reflected in the closing price of fund share. This in turn amplifies the compounding loss effect in the returns due to daily MER deductions.

– Despite this simplification of the model, the differences between the two investment portfolios A and B remain valid. ↩︎