Questrade vs Wealthsimple: Which Is Right for Canadian ETF Investors? (2026)

Quick decision guide

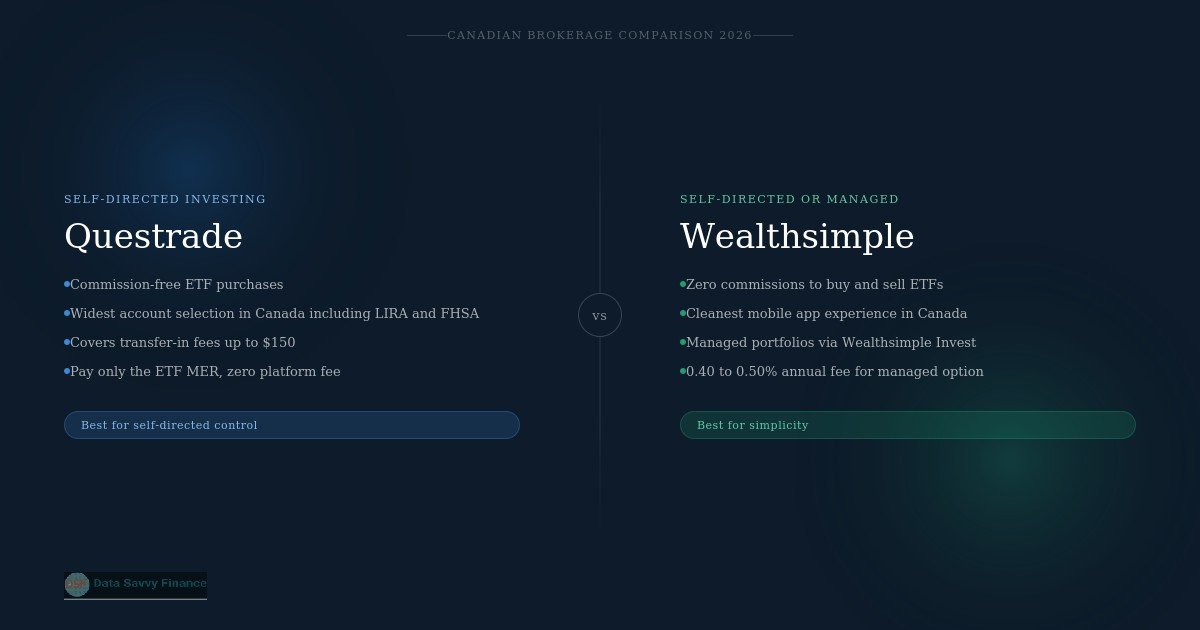

Choose Questrade for self-directed ETF investing with zero buy commissions and the widest account selection. Choose Wealthsimple Trade for commission-free buying and selling in a simple mobile app. Choose Wealthsimple Invest for a fully managed portfolio with no investment decisions required.

This article is for educational purposes only and does not constitute financial or investment advice. The ETFs and platforms mentioned are used as illustrative examples. Before making any investment decision, consider your own financial situation and risk tolerance, and consult a registered financial advisor if needed.

Questrade vs Wealthsimple: Which Is Right for Canadian ETF Investors? (2026)

Here’s something I wish someone had told me earlier: Questrade and Wealthsimple are not really competing for the same investor. They’re built for different people. And once you understand that, the choice gets a lot clearer.

Questrade is a self-directed brokerage. You decide what to buy, when to buy it, and how to structure your portfolio. The platform gives you the tools to execute that plan with commission-free ETF purchases and access to a wide range of registered accounts.

Wealthsimple is two things in one. Wealthsimple Trade is a self-directed app, similar to Questrade but with a simpler interface and commission-free selling. Wealthsimple Invest is a robo-advisor, you answer a risk questionnaire, deposit money, and their team manages the portfolio automatically. You pay for that convenience through an annual management fee.

So the real question isn’t which platform is better. It’s which type of investor you are.

If you want to pick your own ETFs, hold them for decades, and pay as little as possible along the way, Questrade is built for you. If you want to set it and forget it and never think about rebalancing, Wealthsimple Invest is worth looking at. And if you land somewhere in between, Wealthsimple Trade offers a middle ground that’s worth understanding before you decide.

This guide compares both platforms honestly across fees, account types, ease of use, and security, so you can make the right call for your situation.

Questrade and Wealthsimple at a Glance

Before getting into the detailed comparison, it helps to understand what each platform actually is at its core, because the marketing from both companies can blur the picture a bit.

Questrade has been around since 1999 and is Canada’s largest independent discount brokerage. It’s built for self-directed investors, people who want to choose their own ETFs, manage their own asset allocation, and execute trades themselves. The platform gives you the tools to do that at very low cost. Commission-free ETF purchases, a wide range of registered account types, and access to research tools for investors who want them. It’s not the flashiest app on the market, but it’s a serious platform with a long track record.

Wealthsimple launched in 2014 and has since grown into one of Canada’s most recognisable fintech brands. It actually operates two distinct investing products that often get lumped together. Wealthsimple Trade is a self-directed platform, clean, mobile-first, commission-free on both buys and sells. Wealthsimple Invest is a robo-advisor, you complete a risk questionnaire, deposit money, and a managed portfolio is built and rebalanced for you automatically. These are genuinely different products serving different investor needs, and it’s worth knowing which one you’re comparing before drawing conclusions.

One thing both platforms share: they’re legitimate, regulated Canadian brokerages. Both are members of CIPF and regulated by CIRO. Neither is a risky or obscure choice.

For a beginner opening their first TFSA and buying an all-in-one ETF, here’s a step-by-step guide to opening a TFSA at Questrade if you’ve already leaned that direction.

Fees, The Number That Matters Most

Let’s be direct: for a Canadian investor buying and holding low-cost ETFs, fees are the single most important factor in choosing a platform. Not the app design. Not the brand. The fees.

Here’s how each platform stacks up.

Trading commissions

Questrade charges nothing to buy ETFs. That’s a genuine advantage for investors who are regularly adding money to their portfolio, every contribution goes entirely into the market. Selling ETFs costs $4.95 to $9.95 per trade, which matters less for a long-term buy-and-hold investor who rarely sells.

Wealthsimple Trade charges nothing to buy or sell stocks and ETFs. If you’re planning to sell positions at any point, whether to rebalance or to access cash, Wealthsimple Trade has a structural cost advantage here.

For most beginner investors who are in accumulation mode and buying ETFs regularly but rarely selling, the commission difference between the two platforms is effectively zero.

Platform and management fees

Neither Questrade nor Wealthsimple Trade charge monthly account fees. Both have a $0 minimum deposit. For self-directed investors, the platform cost is essentially nothing at both brokerages.

Wealthsimple Invest is different. The managed portfolio service charges 0.50% annually on balances under $100,000 and 0.40% on balances above that. You also pay the MER of the underlying funds, which runs around 0.20%. So the total annual cost for a managed Wealthsimple Invest account is roughly 0.70%, meaningfully higher than self-directing through either platform.

That 0.70% is not outrageous, it’s far below what bank mutual funds charge. But it’s a real cost, and it compounds. On a $100,000 portfolio over 25 years it adds up to a significant difference versus paying only the ETF’s MER.

The investment growth calculator makes that comparison easy to visualize with your own numbers.

Fee comparison at a glance

| Questrade | Wealthsimple Trade | Wealthsimple Invest | |

| ETF buy commission | $0 | $0 | N/A |

| ETF sell commission | $4.95 to $9.95 | $0 | N/A |

| Platform fee | $0 | $0 | 0.40 to 0.50%/yr |

| Minimum deposit | $0 | $0 | $0 |

| Underlying fund MER | Your choice | Your choice | ~0.20% + fee |

For a deeper look at how MER and platform fees compound over time, see what is a good MER for Canadian ETF investors.

Account Types Available

For most beginners opening their first investment account, both platforms cover everything you need. But there are some meaningful differences worth knowing about before you commit.

Questrade offers the widest selection of registered accounts available at any Canadian discount brokerage. TFSA, RRSP, RESP, FHSA, LIRA, LIF, RIF, and non-registered accounts are all available, along with corporate accounts for business owners. The LIRA and LIF options are particularly relevant for anyone transferring a locked-in pension from a previous employer — not every platform supports these, and having to split accounts across two brokerages because one doesn’t support your account type is genuinely annoying.

Wealthsimple covers the core registered accounts, TFSA, RRSP, RESP, FHSA, and non-registered, through both its Trade and Invest products. For the majority of Canadian investors who are primarily working with a TFSA and an RRSP, Wealthsimple covers everything they need. Where it falls short is for investors with locked-in pension funds or corporate accounts who need the broader account range Questrade provides. For example, when it comes to LIF and RIF, both Weatlhsimple and Questrade support both of these account with some subtle differences: Questrade supports both accounts with self-directed and managed, and USD and CAD, while Wealthsimple support only managed (not self-invested) and in CAD (not USD).

The practical takeaway: if you’re a salaried employee opening a TFSA or RRSP for the first time, both platforms work equally well for your account type. If you’re self-employed, have a locked-in pension, or run a corporation, Questrade is the more future-proof choice.

For a clear breakdown of whether a TFSA or RRSP makes more sense as your starting point, this guide to opening a TFSA at Questrade walks through that decision.

Ease of Use, Platform Experience

This is where the two platforms feel most different day to day. And honestly, it comes down to what you actually want from an investing app.

Questrade

Questrade’s platform is functional and data-rich. There’s a web version and a mobile app called QuestMobile, and both give you access to real-time quotes, order types, watchlists, and research tools. It’s not the prettiest interface you’ll ever use, it feels more like a serious financial tool than a consumer app, which is exactly what it is.

The learning curve is real but manageable. Most beginners figure out how to place a basic ETF buy order within their first session. The parts that feel complex, options trading, margin settings, advanced order types, are things a buy-and-hold ETF investor will never touch. Ignore those sections entirely and the platform becomes much simpler.

Wealthsimple Trade

Wealthsimple Trade is genuinely one of the most beginner-friendly investing apps available in Canada. It’s mobile-first, clean, and deliberately stripped back. There are no complex order types, no overwhelming dashboards, no research tools competing for your attention. You search for an ETF, enter the amount, and buy. That’s it.

The simplicity is a feature for some investors and a limitation for others. If you want to dig into fund data, compare allocation models, or set limit orders, Wealthsimple Trade isn’t built for that. If you want to buy XEQT every month and never think about it again, it’s close to perfect.

Wealthsimple Invest

This is the simplest experience of the three by a significant margin. You answer a risk questionnaire, set up a deposit schedule, and Wealthsimple handles everything else — allocation, rebalancing, reinvesting dividends. There are no investment decisions required after the initial setup. For investors who know they won’t stay disciplined during a market downturn without a managed solution, that removal of decision-making has genuine psychological value.

The trade-off is the 0.50% annual management fee. You’re paying for that simplicity, and it compounds just like your returns do, only in the opposite direction.

Which Platform Is Right for You?

This is the section that actually matters. The specs and features are useful context, but what most people really want to know is which platform to open an account with today.

Here’s an honest framework.

Choose Questrade if:

You want to self-direct your ETF purchases and keep every dollar working for you without paying a platform fee on top of the fund’s MER. Questrade is the right choice if you’re comfortable making your own allocation decisions, even a simple one like buying a single all-in-one ETF like XEQT every month.

It’s also the better choice if you’re transferring a mutual fund account from a bank. Questrade covers transfer-in fees up to $150 per account, which removes one of the most common friction points in switching platforms.

I’d also point anyone planning to use Portfolio Visualizer or other analysis tools toward Questrade, the platform’s data access and account structure integrates more naturally with a research-first approach to investing.

Questrade offers both CAD and USD accounts with no fee, while WealthSimple Trade offers a subscription fee of 10$/month for USD holdings (self-managed). Questrade also supports Norbert Gambit, which allows to avoid currency conversion fees. Wealthsimple started rolling out Norbert Gambit feature rolling up in early months of 2026. Conversion fees on WealthSimple are waivable with Premium Account which is achieved once you have $100,000 in assets with WealthSImple (at which point 10$/month fee charged for the USD holdings is waived).

Choose Wealthsimple Trade if:

You want commission-free buying and selling and a cleaner mobile experience. If you’re buying a single all-in-one ETF and you occasionally sell positions to rebalance or access cash, Wealthsimple Trade’s $0 sell commission saves you money compared to Questrade’s $4.95 to $9.95 per sell trade.

It’s also a solid choice if the Questrade interface feels overwhelming and that friction is genuinely stopping you from getting started. A simpler platform you actually use beats a more powerful one that sits unopened. Getting started matters more than optimising the details.

Choose Wealthsimple Invest if:

You genuinely don’t want to make any investment decisions and you know yourself well enough to know that. Some investors will panic-sell during a market correction regardless of their intentions. A managed account that removes the sell button from the equation has real psychological value for those people.

The 0.50% annual management fee is the honest cost of that peace of mind. It’s not a scandal, it’s significantly cheaper than a bank mutual fund, but it’s worth knowing what you’re paying for.

Can you use both?

Some investors do. A common setup is an RRSP at Questrade for the broader account options and transfer fee coverage, and a TFSA at Wealthsimple Trade for the commission-free sells. It works, but it adds complexity to your record keeping and is only worth the effort if the fee savings are meaningful at your portfolio size.

For most beginners just getting started, pick one platform and focus on the habit of investing regularly. The platform choice matters far less than consistency.

Security and Regulation

This is a question that comes up a lot from first-time investors, and it’s a fair one. Handing your money to an app you downloaded six months ago feels different from walking into a bank branch.

Both Questrade and Wealthsimple are regulated by CIRO, the Canadian Investment Regulatory Organization, which is the national self-regulatory body overseeing investment dealers in Canada. Both are also members of the Canadian Investor Protection Fund (CIPF), which protects client assets up to $1 million per account category if the brokerage becomes insolvent. That protection covers your TFSA, RRSP, and non-registered accounts separately, so the coverage is substantial.

Questrade has been operating since 1999, over 25 years without a major security incident. Wealthsimple has been operating since 2014 and is backed by Power Corporation of Canada, one of the country’s largest financial holding companies. Neither platform is a startup taking undue risks with client money.

Both use two-factor authentication, and both encrypt account data in transit and at rest. Standard practice for regulated Canadian brokerages.

The honest reassurance for beginners: these are not risky or obscure platforms. They are legitimate, regulated, and as safe as any Canadian financial institution outside the big banks.

Transferring From Your Bank

If you’re currently holding mutual funds at a big bank and want to move them to either platform, the process is simpler than most people expect.

Both Questrade and Wealthsimple handle the transfer on your behalf. You fill out a transfer form on your new platform, provide your existing account details, and the brokerage contacts your bank directly. You don’t have to call your bank or manage the logistics yourself. The process typically takes 5 to 10 business days.

One important note: transferring a registered account, TFSA or RRSP, does not trigger a taxable event. Your contribution room is preserved and the transfer happens in-kind or as cash depending on whether the receiving platform supports the holdings you’re moving. Please do not do the account transfer manually, as this may trigger taxable event.

On fees: your bank will likely charge a transfer-out fee, typically $100 to $150. Questrade covers transfer-in fees up to $150 per account, which effectively makes the switch free in most cases. Wealthsimple has also offered transfer fee coverage at various points, check their current terms before initiating a transfer as these promotions change.

The bigger win from transferring is getting out of high-MER mutual funds and into low-cost ETFs. See how mutual fund fees compare to ETF fees in Canada for the full cost breakdown.

Conclusion

Both platforms are legitimate, low-cost, and significantly better than leaving your money in a bank mutual fund. The choice between them comes down to one question: how involved do you want to be?

If the answer is fully involved, you want to pick your own ETFs, control your allocation, and pay only the fund’s MER, Questrade is the right platform. Commission-free ETF purchases, the widest account selection in Canada, and transfer fee coverage make it the strongest choice for a self-directed investor.

If the answer is hands-off, you’d rather deposit money and let someone else handle the decisions, Wealthsimple Invest is worth the 0.50% annual fee for the simplicity it provides.

And if you land somewhere in between, you want to self-direct but prefer a cleaner mobile experience, Wealthsimple Trade is a solid middle ground.

Pick the one that matches how you actually invest, not how you think you should invest. Consistency beats optimisation every time.

| Self-directed ETF investing Want full control of your ETF portfolio? Open a commission-free account at Questrade. | Prefer a managed approach? Get started with Wealthsimple and let their team handle the rebalancing. |

Frequently Asked Questions

For absolute beginners who want simplicity, Wealthsimple Trade’s app-first design has a gentler learning curve. For beginners who want to learn self-directed investing with commission-free ETF purchases and access to more account types, Questrade is the stronger long-term platform. Both are legitimate starting points.

No. Questrade offers commission-free ETF purchases. ETF sales cost $4.95 to $9.95 per trade. For a buy-and-hold investor who rarely sells, the effective cost of using Questrade for ETFs is close to zero.

Wealthsimple Trade charges no commissions on stocks or ETFs. Wealthsimple Invest charges an annual management fee of 0.50% on balances under $100,000 and 0.40% above that, in addition to the MER of the underlying funds.

Both platforms are regulated by CIRO and are members of the Canadian Investor Protection Fund (CIPF), which protects client assets up to $1 million per account category in the event of firm insolvency. Both are established, regulated Canadian brokerages.

Yes. Both platforms offer TFSA and RRSP accounts. Some investors hold accounts at both platforms. Your contribution room is personal and not affected by how many brokerages you use.

Yes. Questrade covers transfer-in fees charged by your current institution up to $150 per account. This makes it practical to move mutual fund accounts from a bank without paying the bank’s transfer-out fee out of pocket.

Both platforms have a $0 minimum deposit to open an account. You can fund with any amount you’re comfortable starting with.